Global warming has long ceased to be an abstract threat and most countries have already declared an ambition to reach Net Zero – a state in which CO₂ emissions are fully offset by CO₂ absorption and the net balance becomes zero. It seems that we are heading towards a future of clean energy and green technology. But this beautiful goal hides a paradox: wind turbines, solar panels or electric cars do not arise out of thin air. They are made of metals – copper, lithium, nickel, cobalt, aluminum and rare earth elements.

This is where the climate agenda collides with reality: demand for these metals is growing faster than their supply. More and more scenarios point to impending shortages of copper, lithium and cobalt – already on the horizon of the next decades.

Which metals are becoming critical – and why is the world increasingly constrained not by technology, but by the physical limitations of the material base? What are geologists and geophysicists in the West discussing when they talk about Net Zero, green energy and the future of metals? We explore these questions with Prof. Alan G. Jones (Dublin Institute for Advanced Studies), President of ManoTick GeoSolutions Ltd.

Global warming: a brief history and real consequences

The conversation about global warming started long before it became part of the political and corporate agenda. As early as the late 19th century, scientists proved that carbon dioxide can trap heat in the atmosphere. In the middle of the 20th century, the first systematic measurements of CO₂ concentrations appeared, and these data have been recorded continuously since the late 1950s. They show a simple dynamic: as industry, transportation and energy consumption grow, the concentration of CO₂ in the atmosphere increases steadily, and with it the average temperature on the planet.

Even a slight increase in the average temperature is not “a little warmer in summer”, but a change in the usual living conditions. Heat, which used to be considered abnormal, is becoming a regular occurrence: in cities, it is increasingly impossible to work normally during the day without air conditioning, and the number of heat strokes is increasing, especially among the elderly and children. In winter, on the contrary, the weather becomes less predictable: instead of stable frosts, there are sharp thaws, ice and accidents on the roads.

Water is also changing. In some regions, short but devastating downpours are becoming more frequent, flooding yards, basements and first floors in a matter of hours. In others, prolonged droughts are causing irrigation restrictions, food prices to rise and farmers to suffer. Forest fires are not “somewhere far away,” but a source of smoke that causes schools to close, flights to be canceled, and people to be advised not to go outside.

The bottom line is that climate directly affects the cost of living, health, safety, and stability – so governments and businesses are forced to consider climate risks not because of ideology, but because it becomes too expensive to ignore them.

Glaciers around the world – from the Alps and Rocky Mountains to the Himalayas and Alaska – are rapidly shrinking. According to NASA, this is one of the most visible and measurable indicators of climate change.

Source: NASA, Glaciers Are Retreating

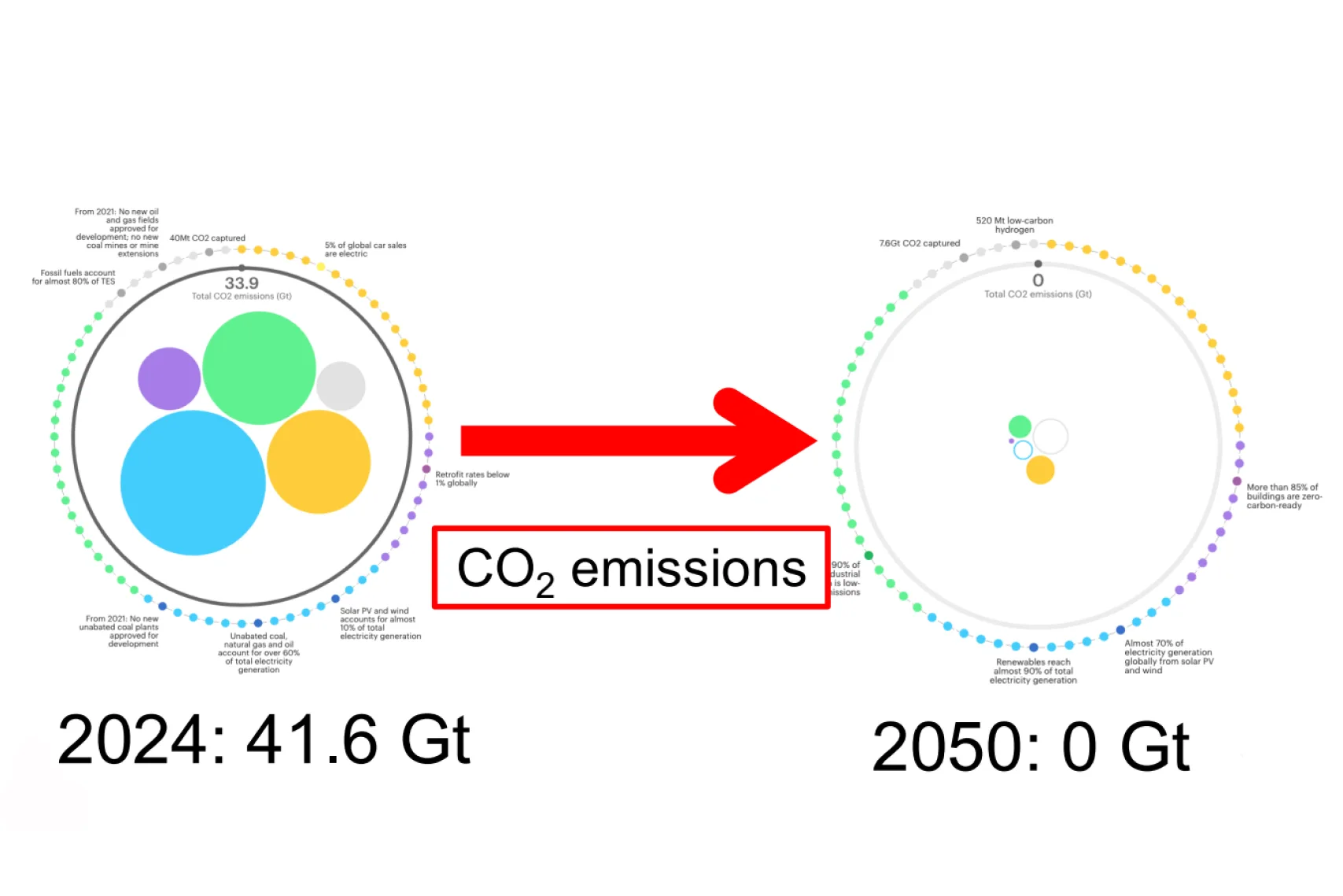

Net Zero target: numbers, timelines and real-world emission trends

The Net Zero goal is to reach zero carbon dioxide emissions by 2050 – a situation in which no additional CO₂ enters the atmosphere. Between 2023 and 2024, humanity emitted about 41-42 gigatons of CO₂ per year, and this means the need to reduce almost all of this volume over the next 25 years – an extremely short time frame by historical and technological standards.

The actual dynamics remain unfavorable. The only notable decline in global emissions over the past decades occurred in 2020 against the backdrop of the COVID-19 pandemic. Already in the following years, emissions not only recovered but also continued to grow. Overall, the global trend in recent years remains upward: total emissions are increasing rather than decreasing.

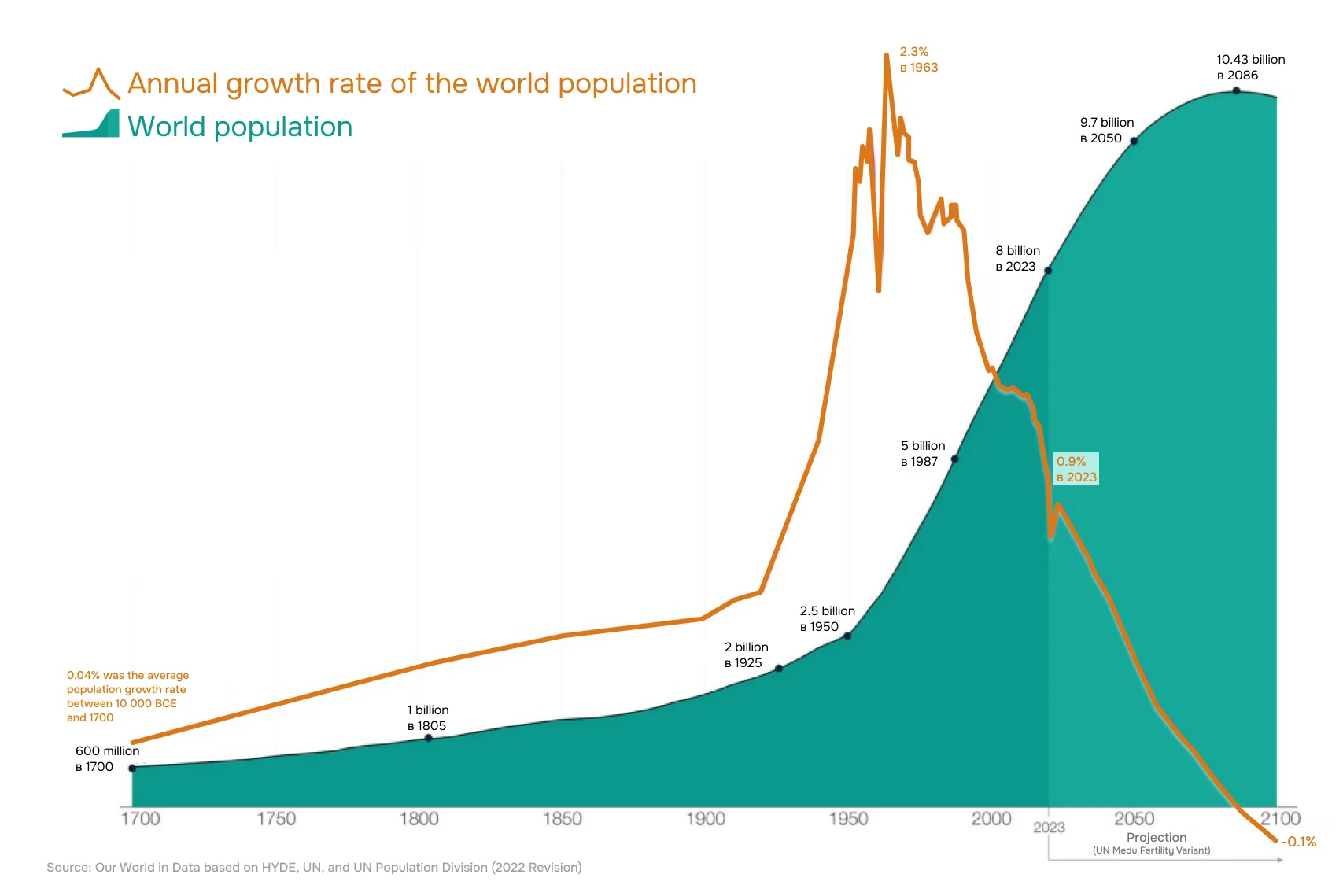

Additional pressure on the climate agenda is being exerted by the growth of the world’s population. According to demographic projections, the world’s population could peak at around 10.5 billion by the end of the 21st century. Population growth is accompanied by an increase in energy consumption, especially in developing countries where rising living standards are directly linked to access to cheap and reliable energy. This means that global energy demand will increase in the coming decades.

In Professor Alan Jones’ assessment, this is the key contradiction in climate policy:

The noble goal of Net Zero faces fundamental limitations. Rising emissions and increasing energy demand against the backdrop of demographic trends are creating a gap between stated climate goals and actual socio-economic processes.

Right: global population growth and slowing growth: demographics remain a key driver of rising energy use and pressure on the climate system.

Climate targets and development scenarios: what’s behind the politicians’ words

Today, most countries in the world have declared climate goals in one form or another. In some cases, states claim to achieve a zero or near-zero carbon balance, usually through a combination of low own emissions and a high share of natural sink ecosystems.

Bhutan and Suriname, which are considered carbon-negative, are commonly cited as examples, as well as Iceland and a number of small countries with limited industrial bases. Dozens of States have set targets for 2030, 2040 or 2045, some for further out, and some have not yet formulated a formal position.

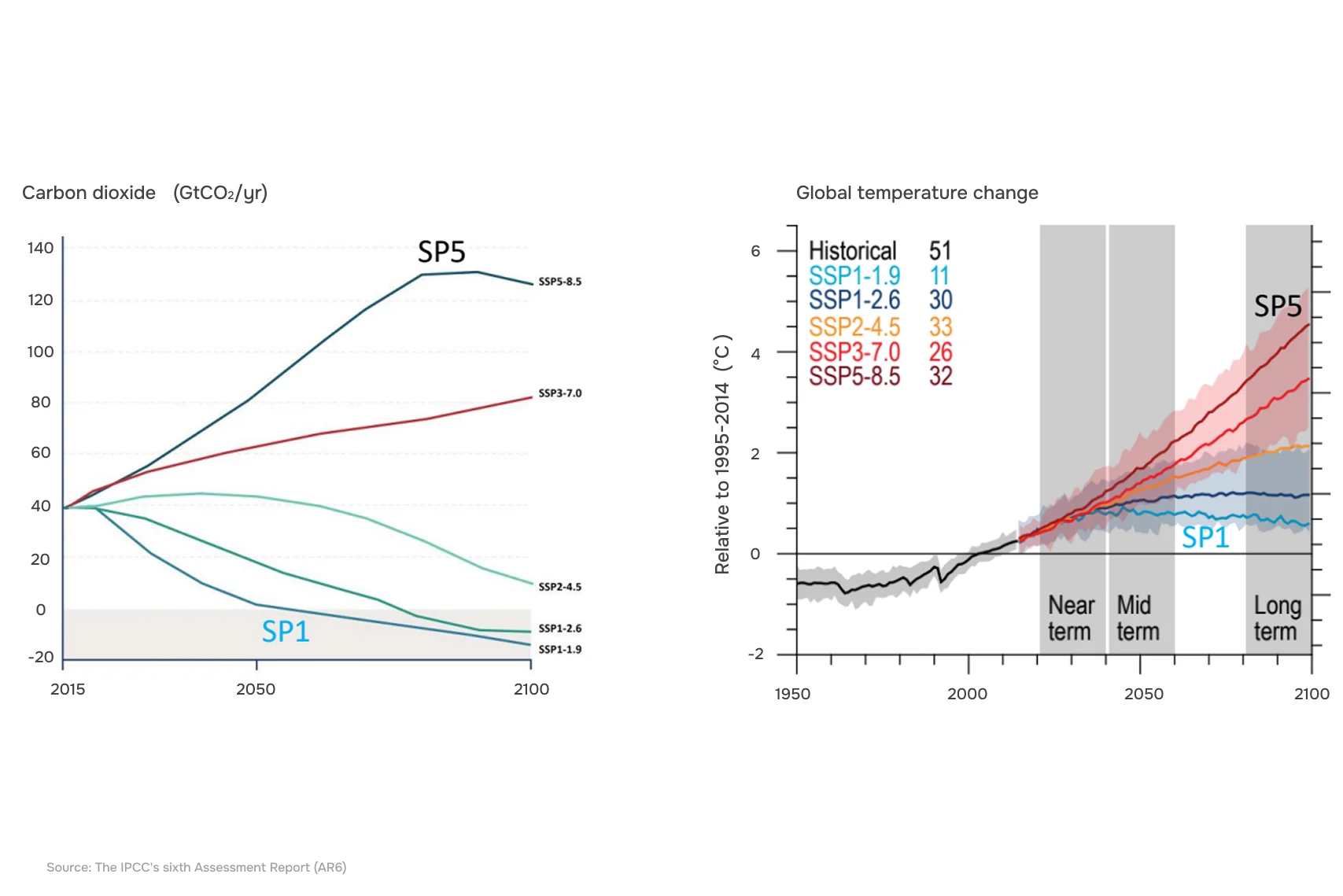

In 2018, the concept of Shared Socioeconomic Pathways (SSP) – ” Shared Socioeconomic Pathways ” – was proposed to analyze how such goals can be realized in practice. This model considers different scenarios of global development – from early and systemic emission reductions to inertial preservation of the current economic and energy structure.

The first scenario is SSP1, or the sustainable development pathway, which the authors themselves call “green”. It assumes early and tough measures to reduce emissions: accelerated closure of coal and gas-fired power plants, rapid growth of wind and solar generation, electrification of transport and large-scale modernization of power grids.

In terms of technology, this scenario looks feasible, but it requires a dramatic overhaul of infrastructure and the way of life within a very short time frame. But this is where the main limitation arises: energy systems, factories and transportation are designed to operate for decades, and their accelerated replacement means high costs, rising energy prices and politically painful decisions.

Therefore, already today the “green” scenario faces strong public and political resistance – from mass protests against tariff increases to slogans about the need to “return to cheap and reliable energy”.

The opposite scenario, SSP5, assumes maintaining the current development trajectory with minimal changes in the economy and energy sector. In this scenario, societal adaptation is easier: there is no need to quickly close existing power plants, drastically change transportation or revise consumption patterns. However, this is where climate goals actually become unattainable.

If the current energy mix is maintained, emissions either continue to rise or decline too slowly to keep warming within stated targets. This scenario is simpler politically, but it virtually guarantees substantial exceeding of climate targets.

The difference between these approaches is evident in the emissions and temperature projections. In the inertia scenario, global emissions continue to rise, and warming could reach about 5 °C by the end of the century. Even with active measures, as Professor Alan Jones points out, it is probably no longer possible to completely avoid temperature increases: current estimates point to the world moving towards around 2.6 °C. Nevertheless, early and systemic action can still limit further temperature increases and mitigate the magnitude of climate impacts.

This means that the question is no longer whether there will be an energy transition, but at what expense and at what rate emissions can be reduced.

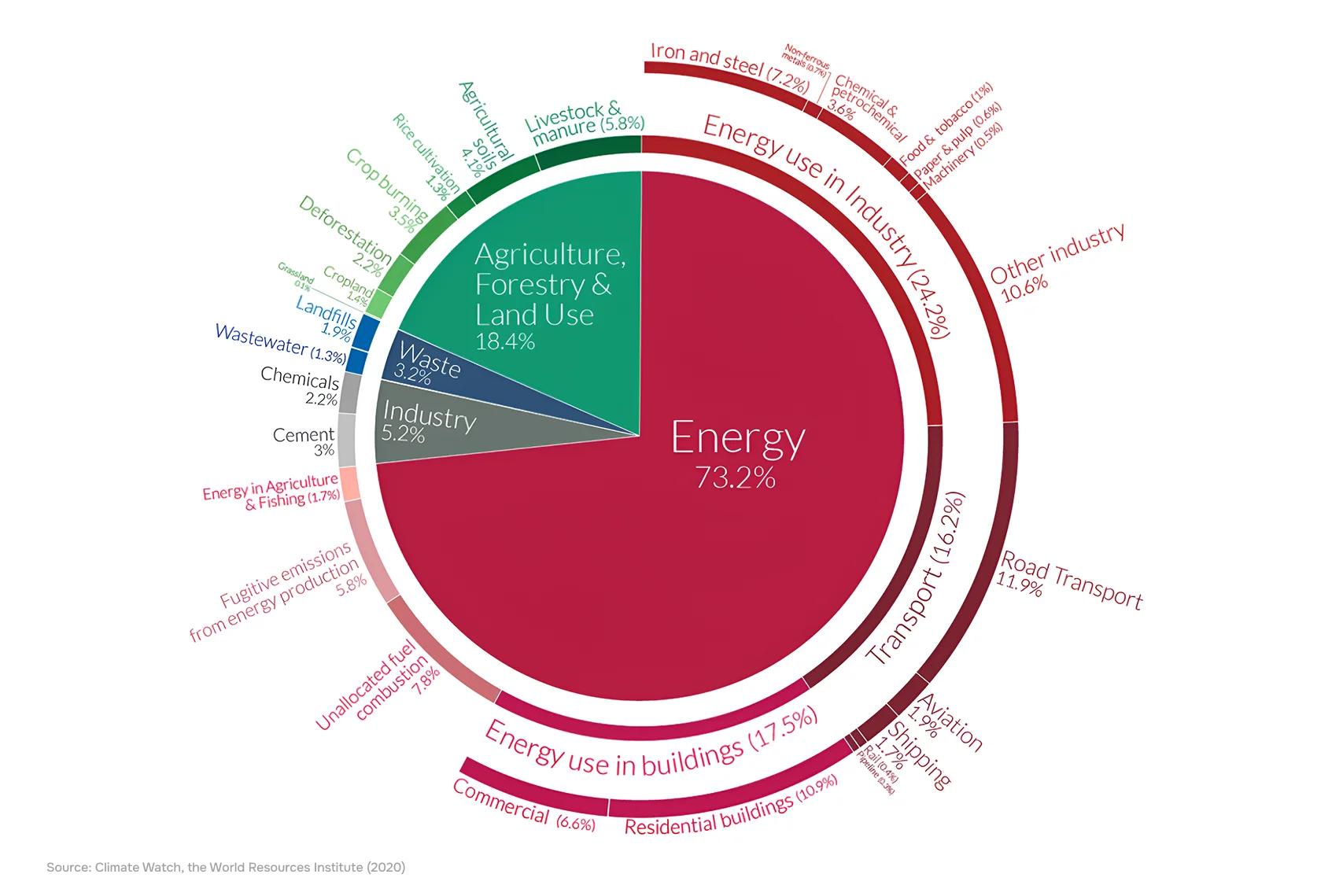

Energy as a key source of emissions

The main source of anthropogenic carbon emissions is the energy sector. It accounts for about 70-75% of global CO₂ emissions. This includes energy used in industry, transportation, electricity and everyday life – from heating buildings to charging our devices. Other sectors also make a notable contribution. Agriculture, forestry and land use account for around 18-20 % of emissions, with industrial processes and waste contributing another 5-10 %.

However, the energy sector remains the largest and systemically important source of emissions. Without its transformation, it will be impossible to achieve the climate goals.

Looking deeper, within the energy industry itself, the distribution is as follows:

- the largest share is in electricity and heat production;

- transportation – cars, trucks, aviation and shipping – gives about 20-25%;

- about 20% more is related to industrial energy consumption.

That’s why the climate agenda almost always boils down to the same set of solutions: abandoning the burning of coal, oil and gas in favor of wind and solar generation, electrification of transportation and large-scale construction of new energy infrastructure.

At the level of ideas, this model looks attractive. Renewable energy sources can reduce direct CO₂ emissions, and electrification of transportation can reduce dependence on fossil fuels. However, there is a side to this transition that is much less often the focus of public debate – the material side.

The material side of green energy

The energy transition is not only about energy sources, but also about physical objects: wind turbines, solar panels, electric cars, batteries, and power grids. All of them require large volumes of metals and minerals, which means a large-scale increase in demand for resources, without which green energy simply cannot exist.

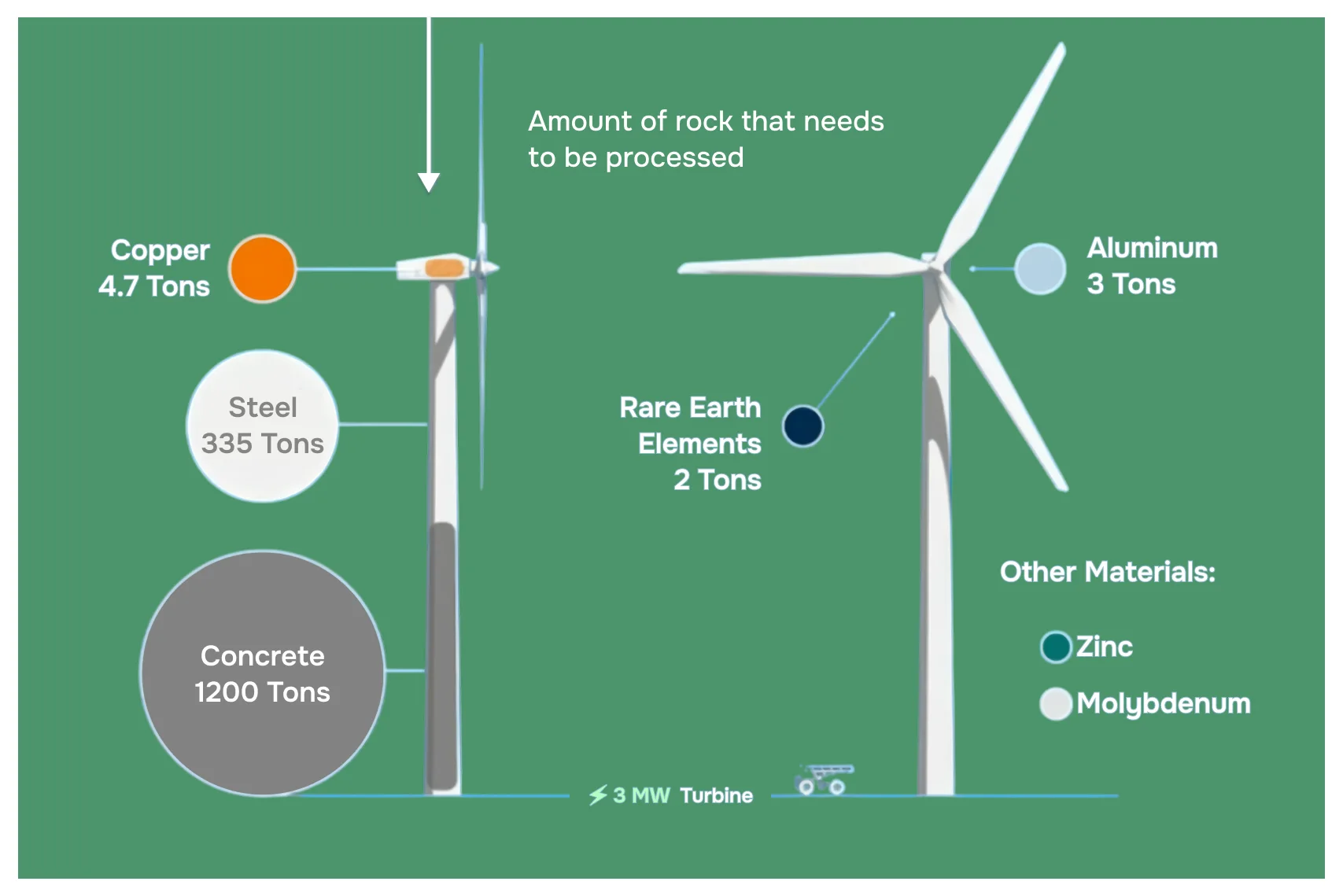

One of the most obvious examples is wind farms. The production of a single wind turbine requires a significant amount of extraction already at the stage of obtaining raw materials:

- To get the rare earth elements needed for a single wind turbine, about 2 tons of rock must be extracted;

- to produce aluminum – another 3 tons of rock;

- for copper, about 5 tons of rock.

In other words, tens of tons of rock mass must be extracted just for one – one – wind turbine. These figures allow us to visualize the scale of extraction required to build all the wind turbines needed for the scenario of keeping global warming below 2 °C.

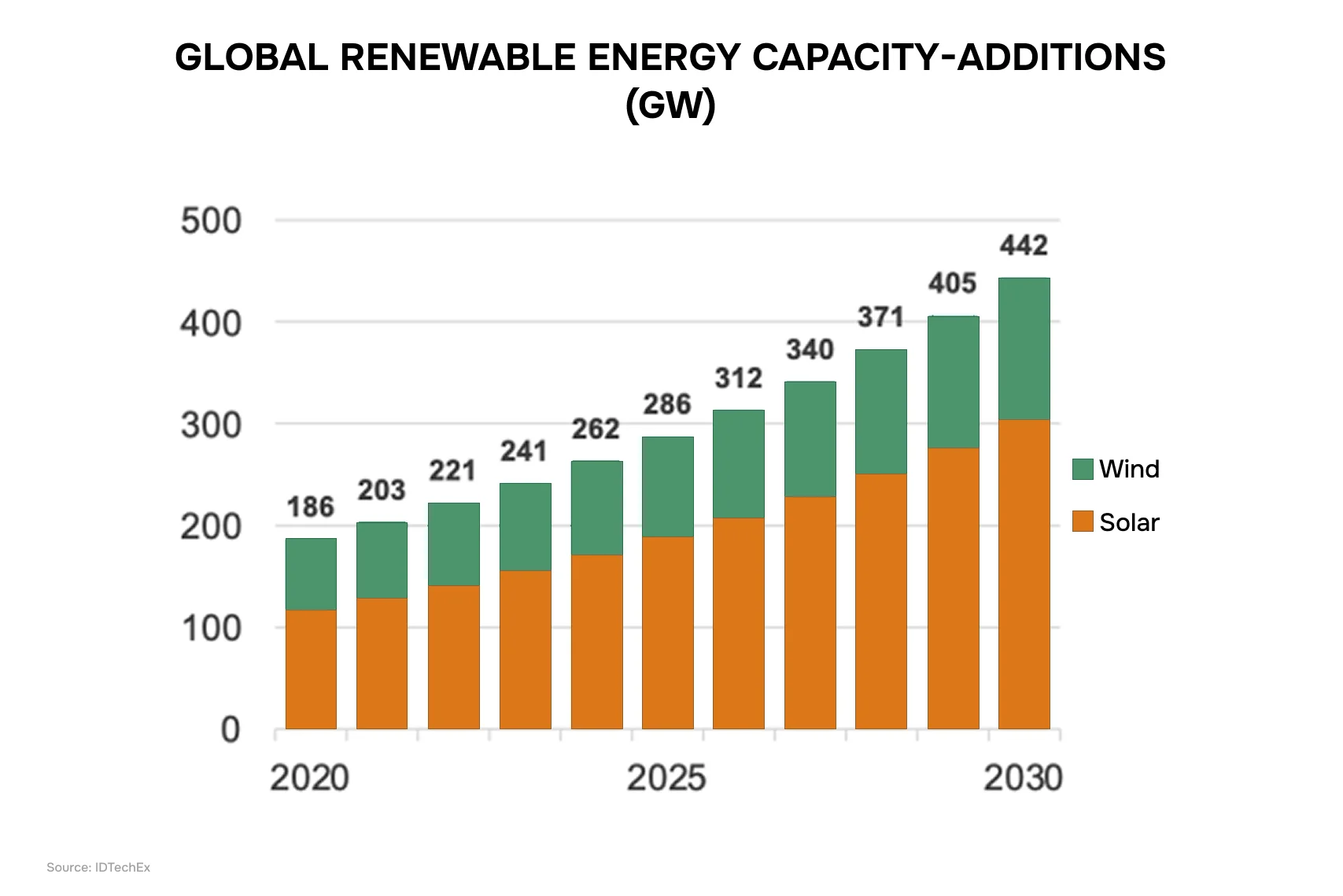

The increase in scale becomes even more evident when looking at projections for new renewable energy capacity additions. According to estimates based on 2020 data, the wind and solar power plants already planned at that time were expected to provide almost three times the installed capacity.

Right: growth in installed solar and wind power capacity globally through 2030.

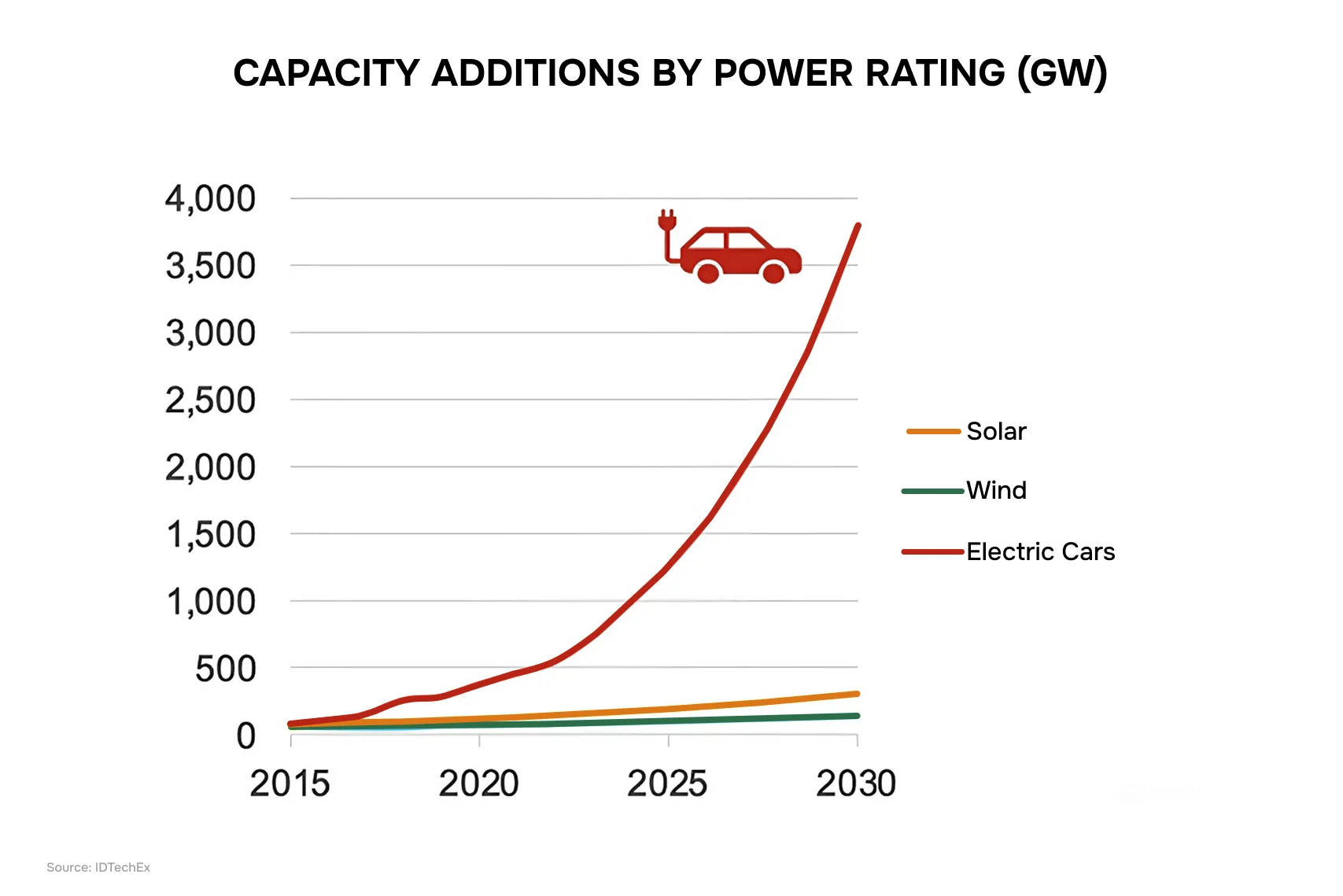

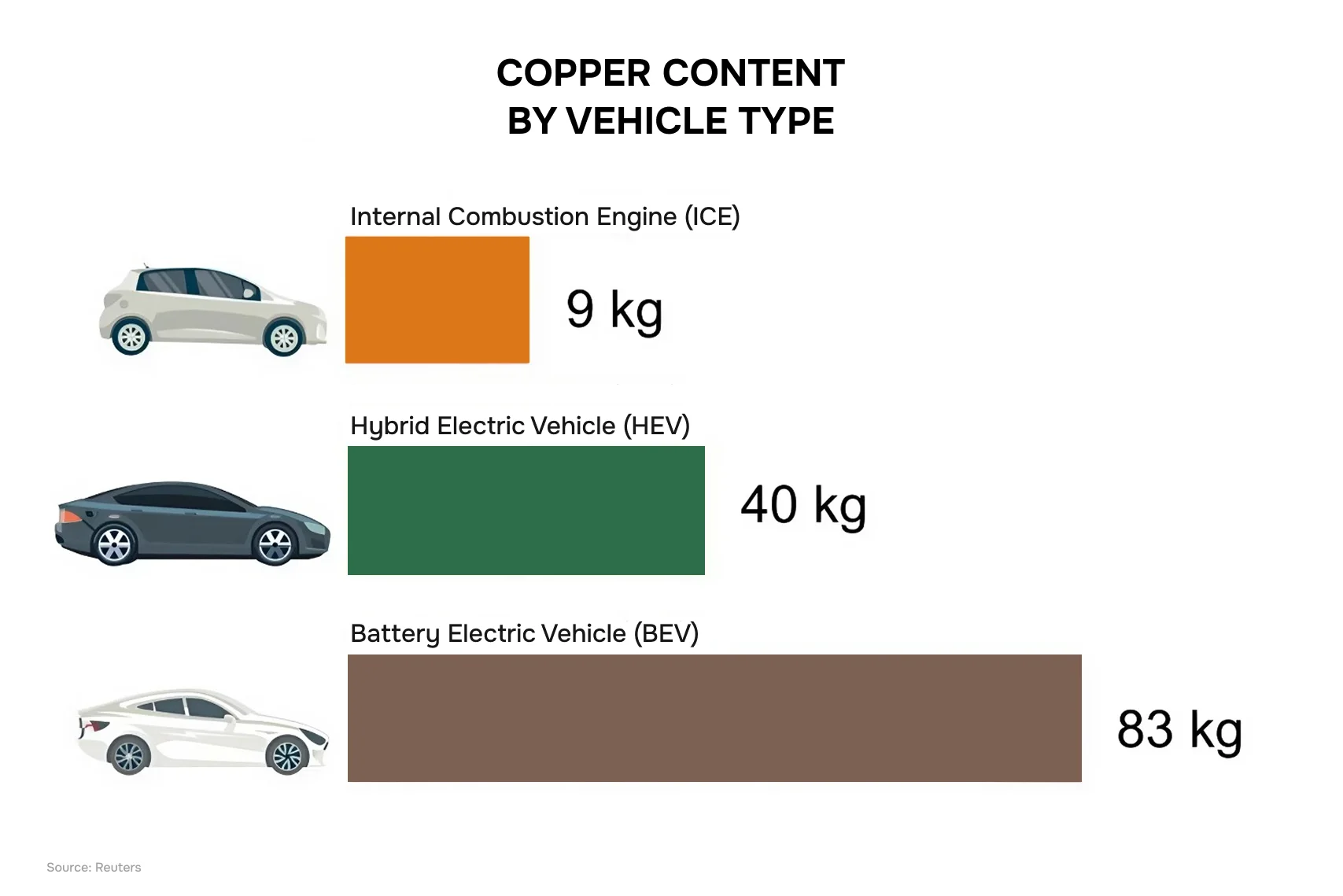

However, with the mass transition to electric transportation, the picture changes radically. The increase in energy consumption associated with electric vehicles is many times greater than the contribution of wind and solar power combined – by a factor of about ten. Electrification of transportation means not only an increase in energy consumption, but also a dramatic increase in the demand for materials. The reason for this is the high material intensity of the vehicles themselves, primarily for key metals such as copper

For comparison:

- a car with an internal combustion engine contains about 9 kg of copper;

- hybrid car – about 40 kilograms;

- battery electric vehicle – about 83 kilograms of copper.

Thus, an electric car requires almost ten times more copper than an internal combustion engine car.

Today, there are about 1.4 billion vehicles in operation in the world – about 1 billion passenger cars and about 400 million trucks and buses. With an average vehicle life of about 14 years, this translates into the production of about 100 million new vehicles per year, as evidenced by the statistics of the pre-pandemic years.

Assuming that all of these cars will be electric, just to produce them would require about 15 megatons of copper annually. At the current copper conversion rate of about 55%, which is already considered high and cannot be drastically increased, this means that about 7 megatons of new copper would need to be mined per year – just for electric cars.

Right: the shift to electric transportation is radically increasing the demand for copper, one of the key metals of the energy transition.

How much copper does a “green” crossing need

The Net Zero-2050 roadmap contains a whole set of intermediate goals and milestones. It is already obvious that it will be extremely difficult to fulfill them. Thus, according to this plan, by 2030, 60% of all new cars hitting the roads should be electric (60 million cars).

To realize this goal, about 4 megatons of new copper per year will be needed by 2030 – on top of what is being produced today. This raises a key question: how much copper are we producing now and how much will we actually need?

If we take into account the expected growth of copper consumption in solar power from 0.6 to 2 megatons per year, as well as demand from onshore and offshore wind power, the combined demand from these sectors rises from about 1 to 3 megatons per year. Even assuming that half of this could be covered by recycling, there remains a need to mine about 1 megatonne of new copper annually for solar and wind generation alone.

A separate and often underestimated item is energy infrastructure. Today, about 150 megatons of copper are “sewn” into the world’s power grids, and the service life of such infrastructure is about 40-45 years. This means that about 20 megatons of grid copper will need to be replaced by 2030, and another 20 megatons by 2040.

As a result, the summarized picture is as follows:

- about 7 megatons of copper a year is required for electric cars;

- another 1 megaton for solar and wind power;

- about 2 megatons to upgrade the power grid.

Total – about 10 megatons of copper per year for these areas alone. For comparison, today’s global copper production is about 21-22 megatons per year. However, in order to cover the needs already listed, production needs to be increased to at least 30 megatons per year – and this is without taking into account other sectors of the economy.

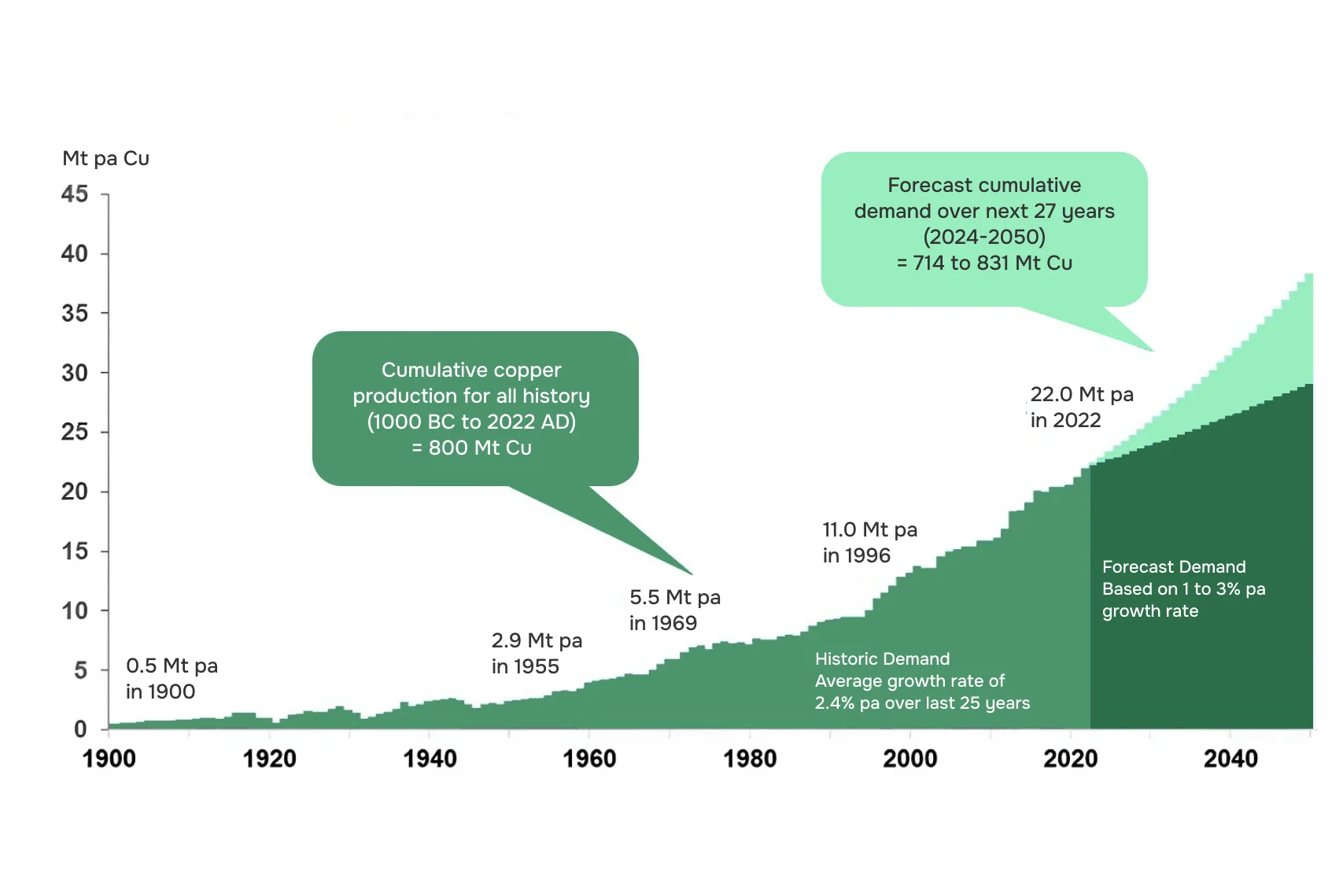

Historical dynamics only amplify the scale of the problem. Global demand for copper nearly doubles every 20-30 years. According to various projections, global production is expected to grow to about 35 megatons by 2035 and to 40-50 megatons per year by 2050.

In other words, humanity will have to mine more copper in the next 25 years than has been mined in all of previous history – if we really intend to get anywhere near Net Zero’s goals at least in terms of a single, but key metal.

Critical metals: the resource side of the energy transition

The energy transition is changing not only the consumption of individual metals, but also the very structure of demand for mineral resources in general. Modern energy and digital technologies are no longer based on a limited set of “classical” materials, but on dozens of elements of the periodic table – from basic to rare and technologically specific.

This is why in recent years the concept of “critical metals and minerals ” – elements without which neither the development of low-carbon energy nor the maintenance of modern technological infrastructure is possible – has gained a foothold on the international agenda.

Back in 2017, different countries had different definitions of what elements were considered critical. The United States, the European Union, Japan and Australia had their own lists, which differed markedly from each other.

However, there has been a rapid consolidation of approaches over the years. By 2025, the lists of critical metals for the US, EU, Japan, Australia and Canada have almost coincided. Researchers estimate that more than half – and in some studies up to two-thirds – of the entire Mendeleev table is now categorized as critical metals and minerals.

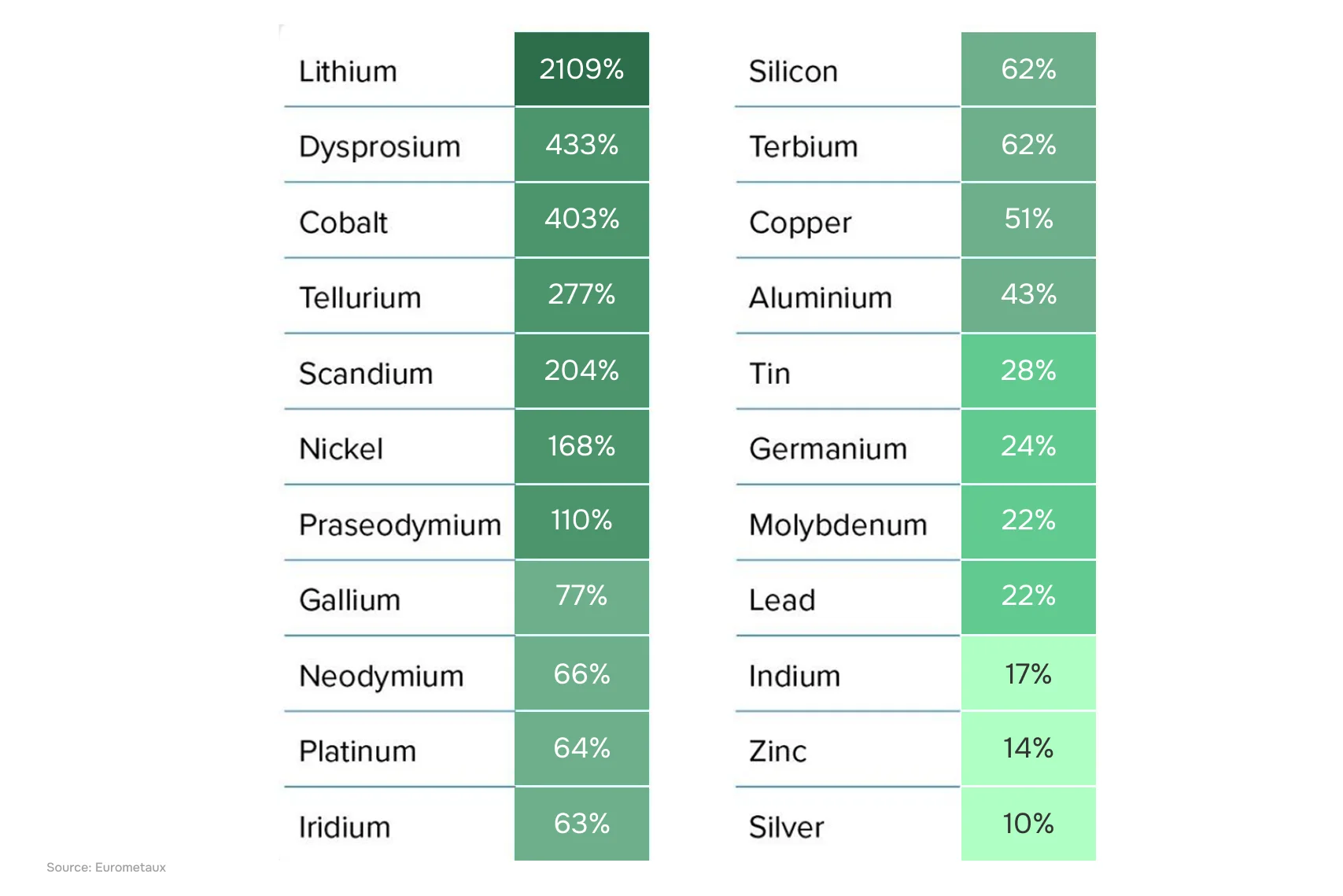

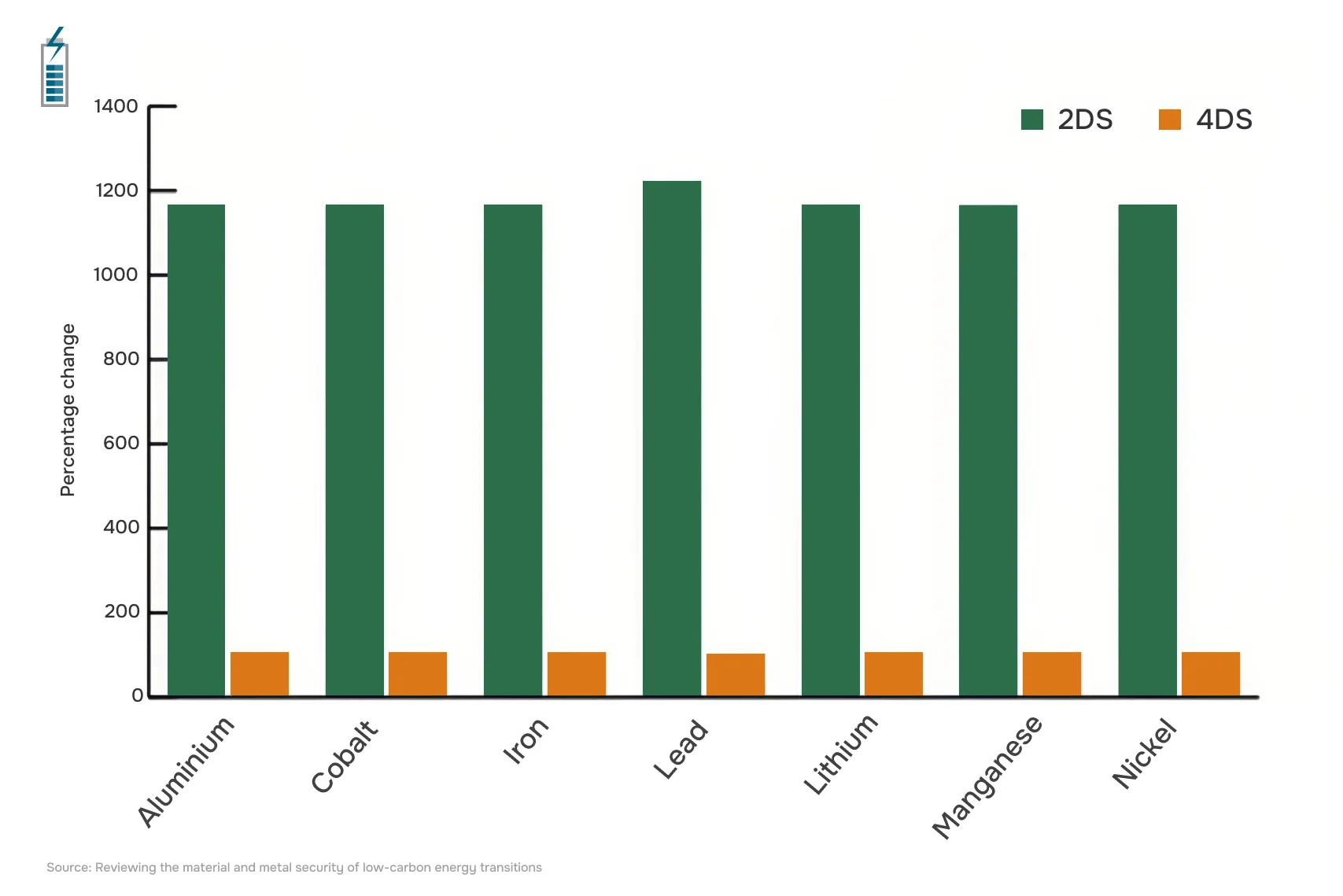

According to various estimates, in order to realize scenarios to curb global warming, lithium extraction needs to increase about 20 times compared to current levels, cobalt – 4 times, and copper, nickel, manganese and a number of other elements also require a multiple increase. Specific figures vary from study to study, but the conclusion is the same: the needs are growing not gradually, but by leaps and bounds.

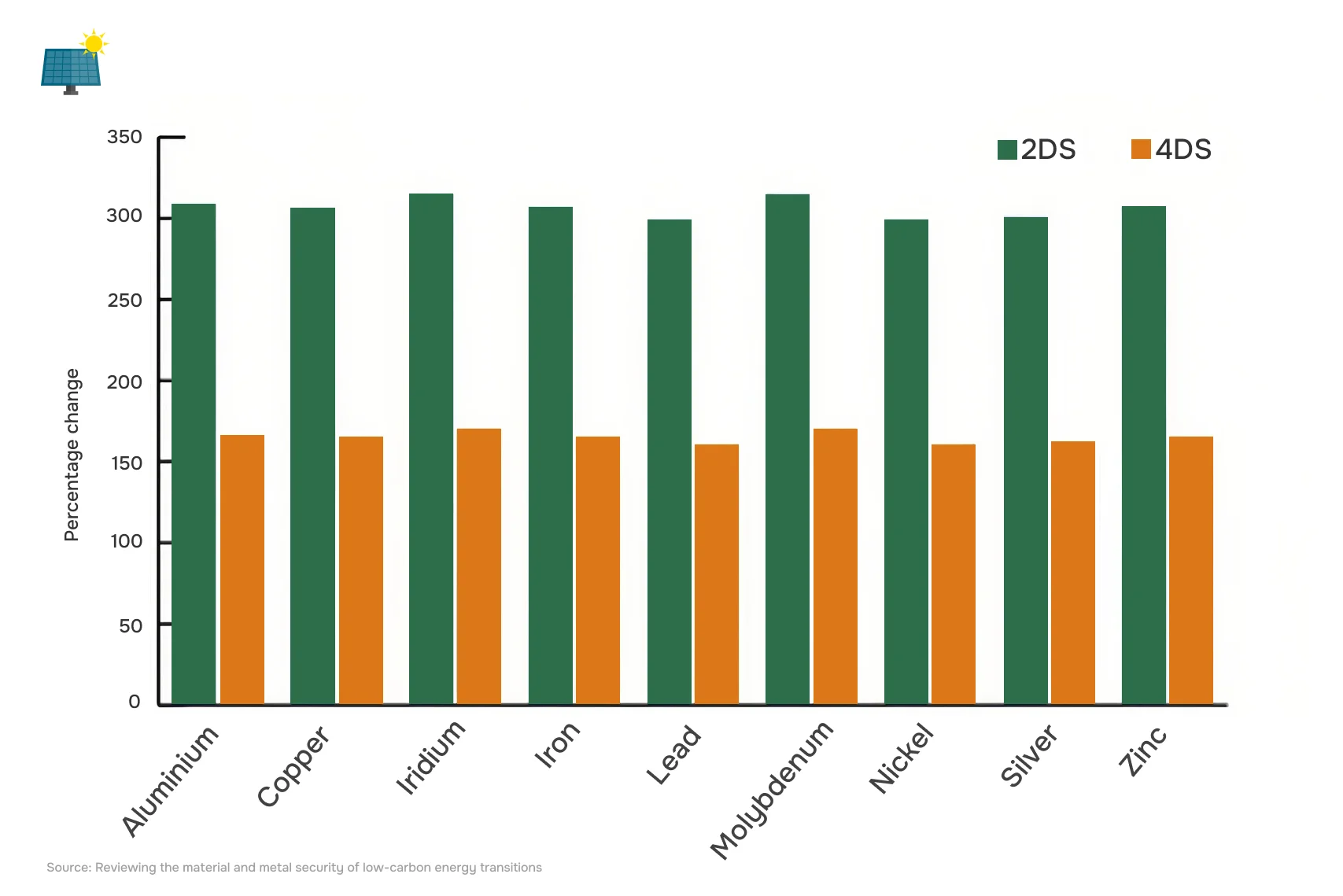

This is particularly evident in energy storage and renewable generation technologies. To produce the lithium-ion batteries needed in a warming scenario below 2 °C, many times more aluminum, copper, lithium, nickel, and manganese will need to be mined than today. The situation is similar in solar energy: without a multiple increase in the extraction of aluminum, copper, indium and other elements, the energy transition is unattainable.

Thus, the issue of critical metals is not a private problem of individual elements, but a structural challenge to the energy transition as a whole.

Right: Growth in metal demand for solar energy – production of photovoltaic panels and related infrastructure.

Recycling doesn’t save the day

At first glance, it may seem that the shortage of critical metals can be solved by recycling. However, in reality, the potential for recycling is quickly overwhelmed by physical and technological limitations.

For copper, the recycling rate today is about 55% – and this is already close to the practical ceiling. It is virtually impossible to significantly increase this share in the coming decades: most copper is permanently “locked up” in infrastructure – power grids, buildings, transportation – with a lifecycle of tens of years.

With other critical metals, the situation is even more complicated. Many of them:

- or no recycling at all,

- or are lost during use and disposal due to low concentrations and technological limitations.

Even under the most optimistic recycling scenarios, the models show that:

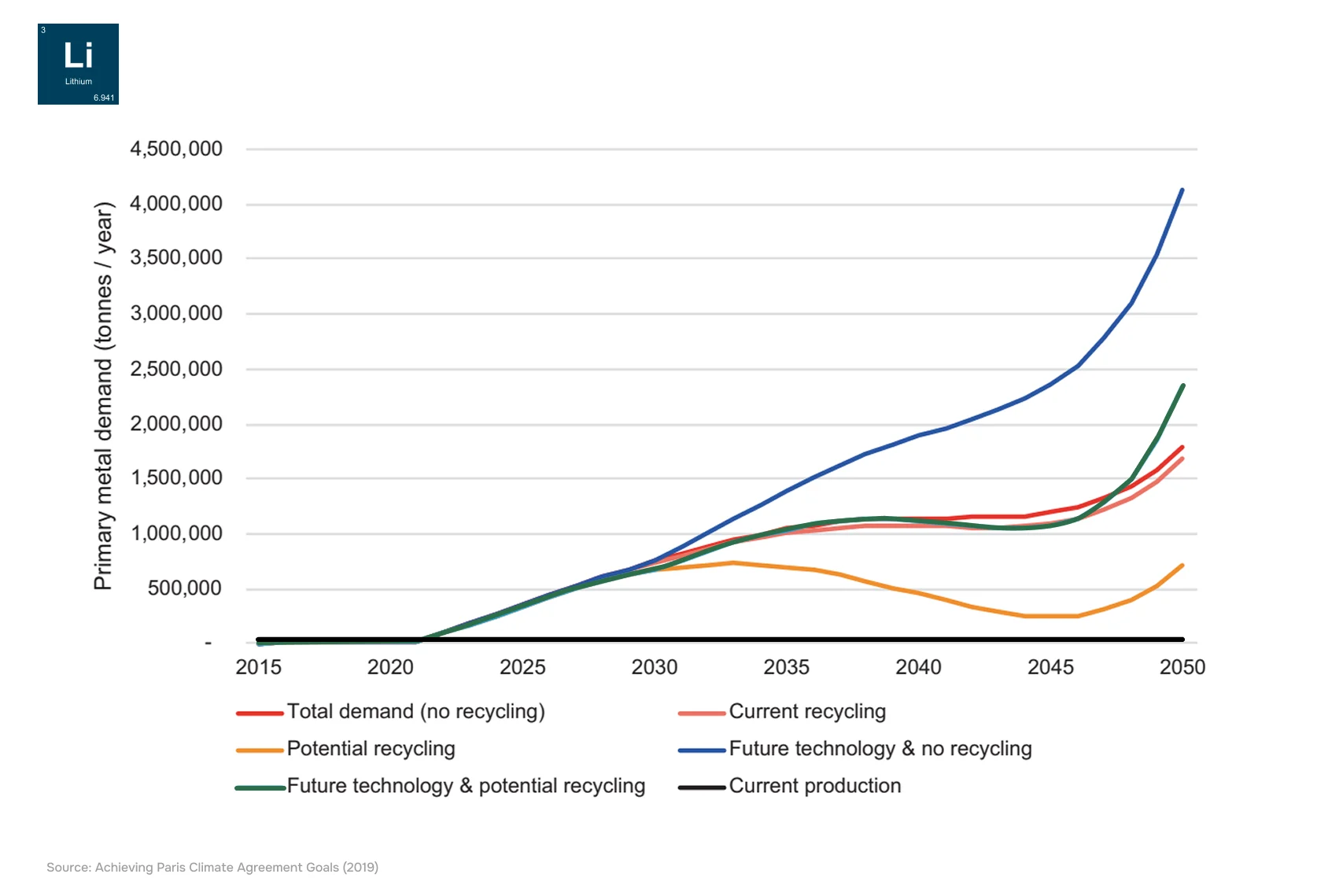

- lithium shortages become likely as early as 2030-2035,

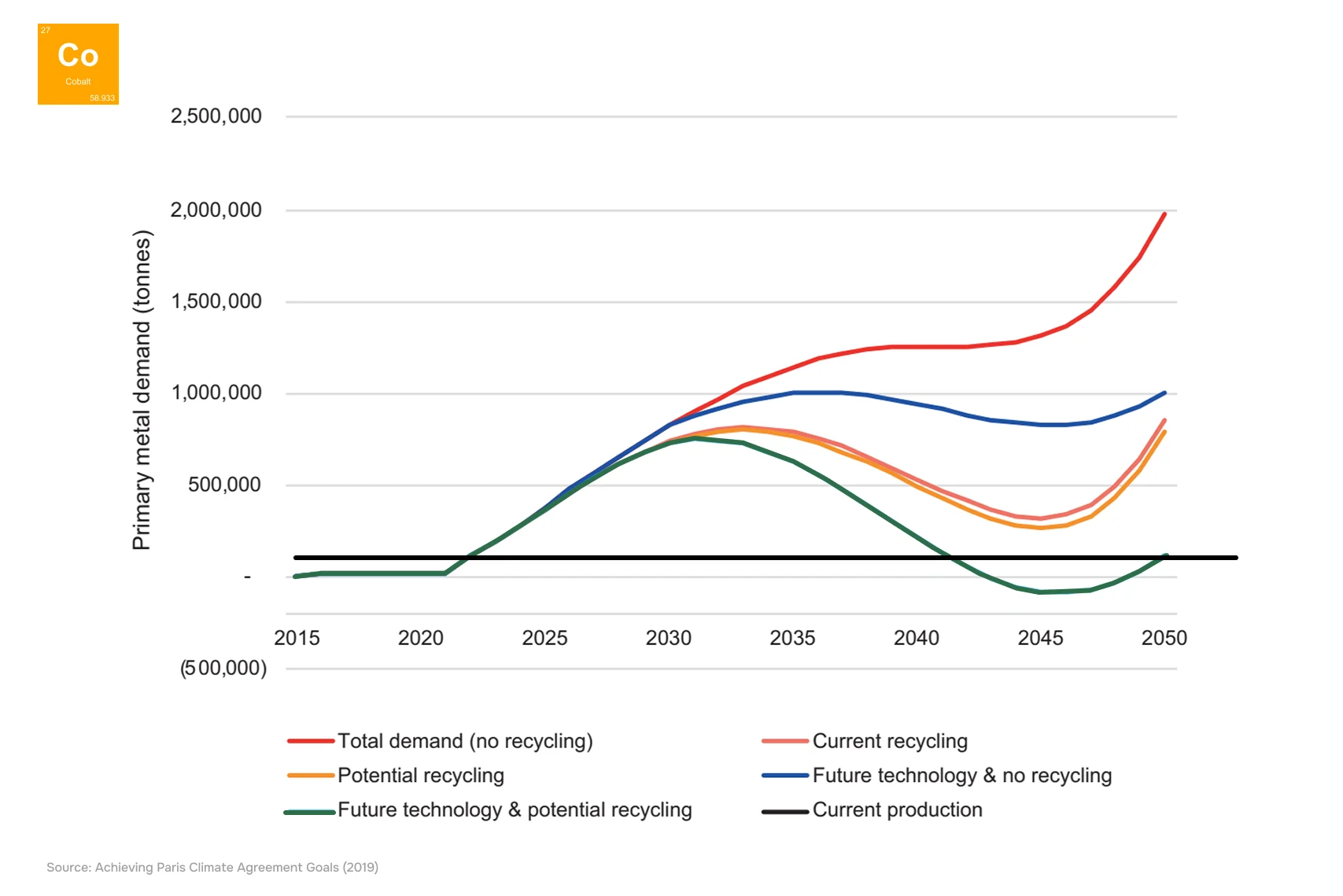

- cobalt shortages are expected between the mid-2020s and 2040.

In other words, recycling can only partially mitigate the problem, but cannot replace the need to find and extract new deposits. In the context of the energy transition, recycling is an auxiliary tool, not a systemic solution.

Without metals, there will be no new economy

Global warming is recognized as a scientific fact and energy is the main cause of it. That is why the world talks about Net Zero and the energy transition. However, behind these formulas is a simple physical reality. Wind turbines, solar panels, electric cars, batteries and new power grids are made up of specific metals. They cannot be “assigned” by political decision, replaced by declarations, or compensated for by recycling alone.

These technologies do not appear out of thin air and do not exist forever: they need to be constantly produced, updated and scaled up. And that means mining the metals they are made of over and over again. Even with maximum recycling, the world will inevitably face shortages of copper, lithium, cobalt and other critical elements in the coming decades. All scenarios agree on one thing: without new deposits, the energy transition is physically impossible.

The energy transition is a resource project. It requires not only new technologies and climate strategies, but also a large-scale, systematic increase in the mineral base through exploration, production and responsible subsoil use.

In the next article, we address the main practical question: how much will the world really have to increase production, where can these resources be found, and who will be able – or unable – to provide this growth.

Cover photo: A farmer at a solar power plant in Weining Autonomous County, Guizhou Province, China, July 3, 2025. Source: Xinhua / Tao Liang