People are buying more smartphones, laptops and home appliances, cities are switching to “smart” systems, and the development of artificial intelligence requires the construction of more and more data centers and server farms that run around the clock and consume enormous amounts of energy. All this infrastructure – from charging stations and power grids to servers and batteries – requires a dramatic increase in the material base – primarily metals.

At the same time, these metals do not come out of thin air. They must be found in the subsurface and mined – a process that is long, risky and takes decades. And this is where a key contradiction arises. On the one hand, the world claims an unprecedented growth in demand for metals. On the other hand, the attitude towards mining remains predominantly negative. Suffice it to recall the words of UN Secretary-General António Guterres at COP26:

“Stop treating nature like a toilet. Stop burning, drilling and digging deeper and deeper into the spoils. We are digging our own grave.”

In this article, join geophysicist Alan G. Jones for a sequential look at where and how new deposits are being sought, how fast they can be brought into production, and what exploration strategies China, Australia, and Canada are using today. How humanity can meet the growing demand for metals without violating environmental and ethical rules. And the final key question is whether the world has the people to put it all into practice.

From mineralization to mine: why new deposits are in short supply

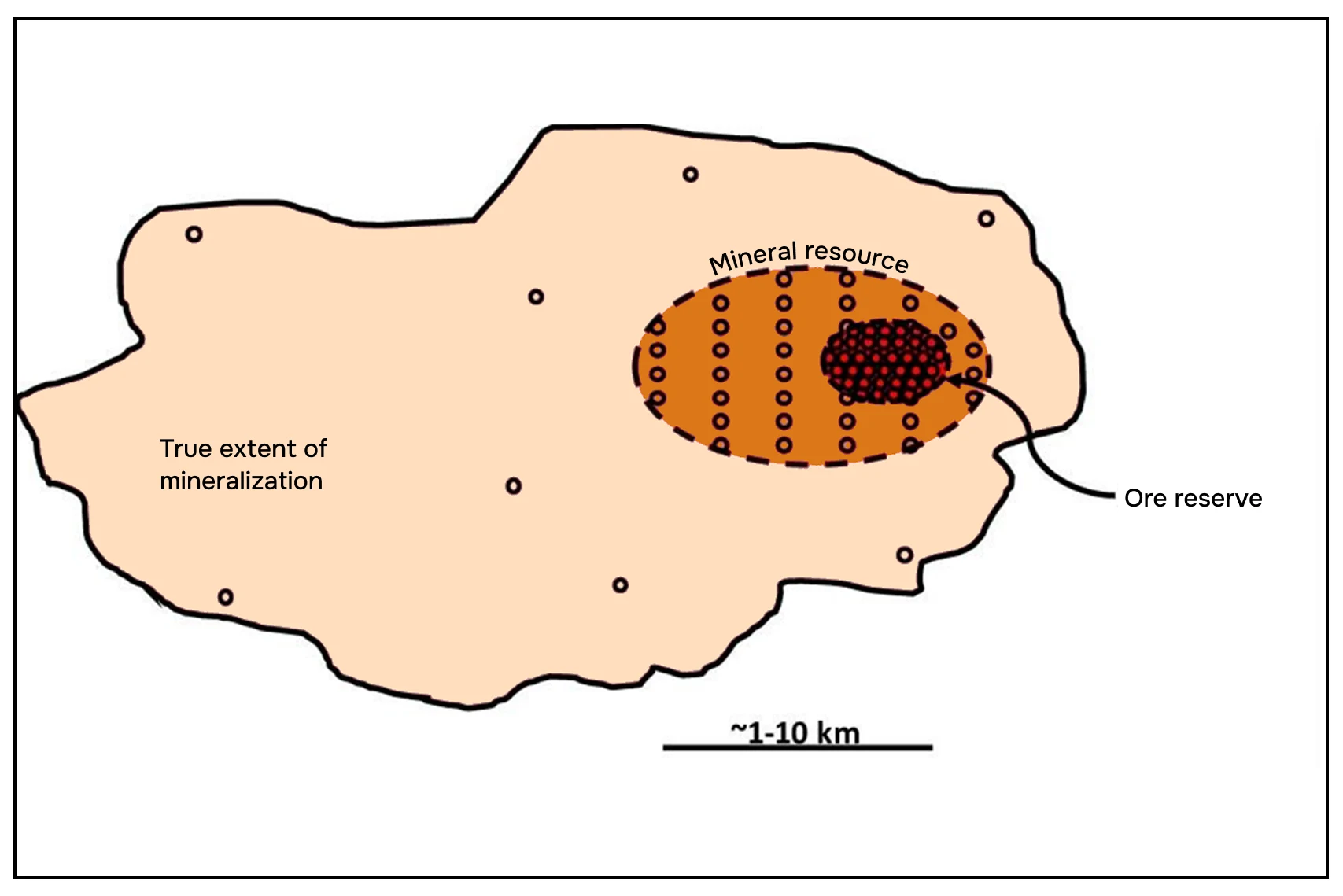

The process of deposit development begins with mineralization – a broad zone in which a useful component is present. Within it is the mineral resource – the already estimated and quantified part. And only within the resource is the ore reserve – the portion that can be mined economically at current technologies and prices.

The key point here is that the size of an ore reserve is directly related to the price of the metal. Mineralization may be well understood, but remain a “mere resource” if it is unprofitable to develop at the current price. When prices rise – for example, when they double – the zone of economically recoverable reserves expands, and the ore reserve formally increases. It is important to understand: metals in the ground at a particular site are not divided into “is” and “is not” – they are divided into “profitable to mine” and “not profitable yet”.

In the same deposit, there may be areas with high metal content and areas with low metal content. As long as the price of metal is low, companies develop only the “richest” areas – those where mining pays off. Everything else is formally considered a resource, but not a reserve: there is metal there, but it is too expensive to get it.

Rising prices are really pushing the boundary of economically recoverable reserves. You can process poorer ores, go deeper, apply more sophisticated technologies. On paper, this looks like an increase in available reserves – although no new deposits appear in the ground.

It is important to understand: price affects the accounting of reserves, but not the speed of exploration. It does not create new targets, accelerate their discovery, or shorten the path from discovery to production. Therefore, rising prices can postpone metal shortages, but they cannot eliminate them in a short period of time.

Why new mines don’t appear “on demand”

Even allowing for rising prices and formal expansion of reserves, the actual production system is constrained by physical and time constraints.

The first problem is the depletion of operating mines. The 200 or so large copper mines that currently provide the bulk of the world’s production will reach the end of their productive life by 2035. This means that even if current demand continues, global copper production will begin to decline – simply because existing mines are being depleted faster than new mines are being built.

The second problem is the decline in ore quality. At the largest porphyry deposits, primarily in Chile, the average copper grade has declined by about 30% over the past two decades. To get the same amount of metal, more and more rock has to be processed. This means higher costs, energy consumption and environmental burdens – even without increasing production.

The third bottleneck is the lack of new projects. There are only about 36 copper projects in the global “pipeline” at the pre-development stage. In total, they are capable of producing only about 2 megatons of additional copper per year, while the world will need to increase copper production by 20-30 megatons per year in the coming decades to realize energy transition scenarios. The gap between demand and capacity is systemic.

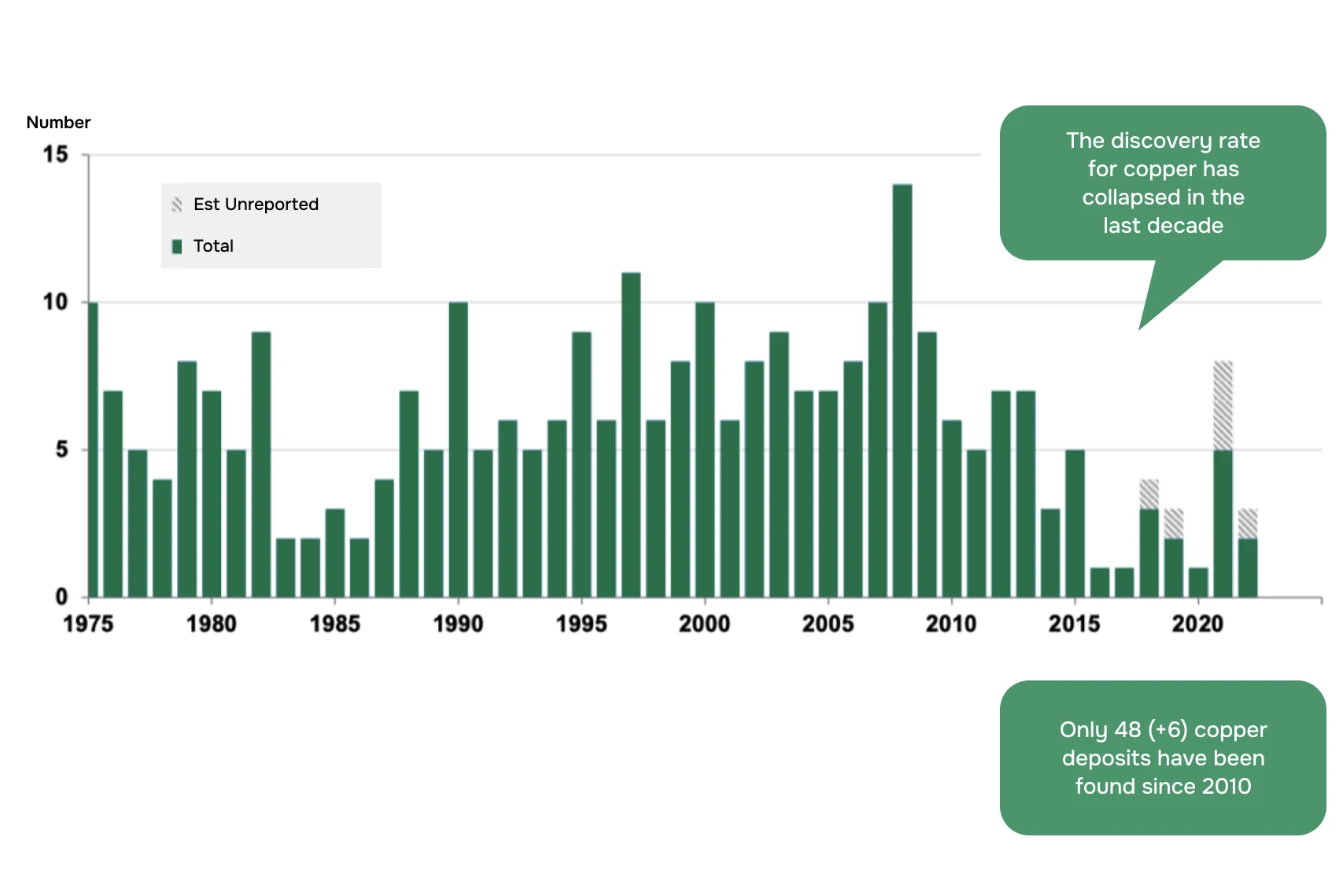

At the same time, exploration rates remain extremely low, with only 46 new copper deposits discovered globally since 2010.

On average, only one out of about 3,000 mineralized occur rences – areas where geologists record the presence of copper – eventually turns into an operating mine. That translates into a success rate of about 1 in 3,000. Most sites are either too small, too poor, or too geologically, environmentally, logistically or economically challenging.

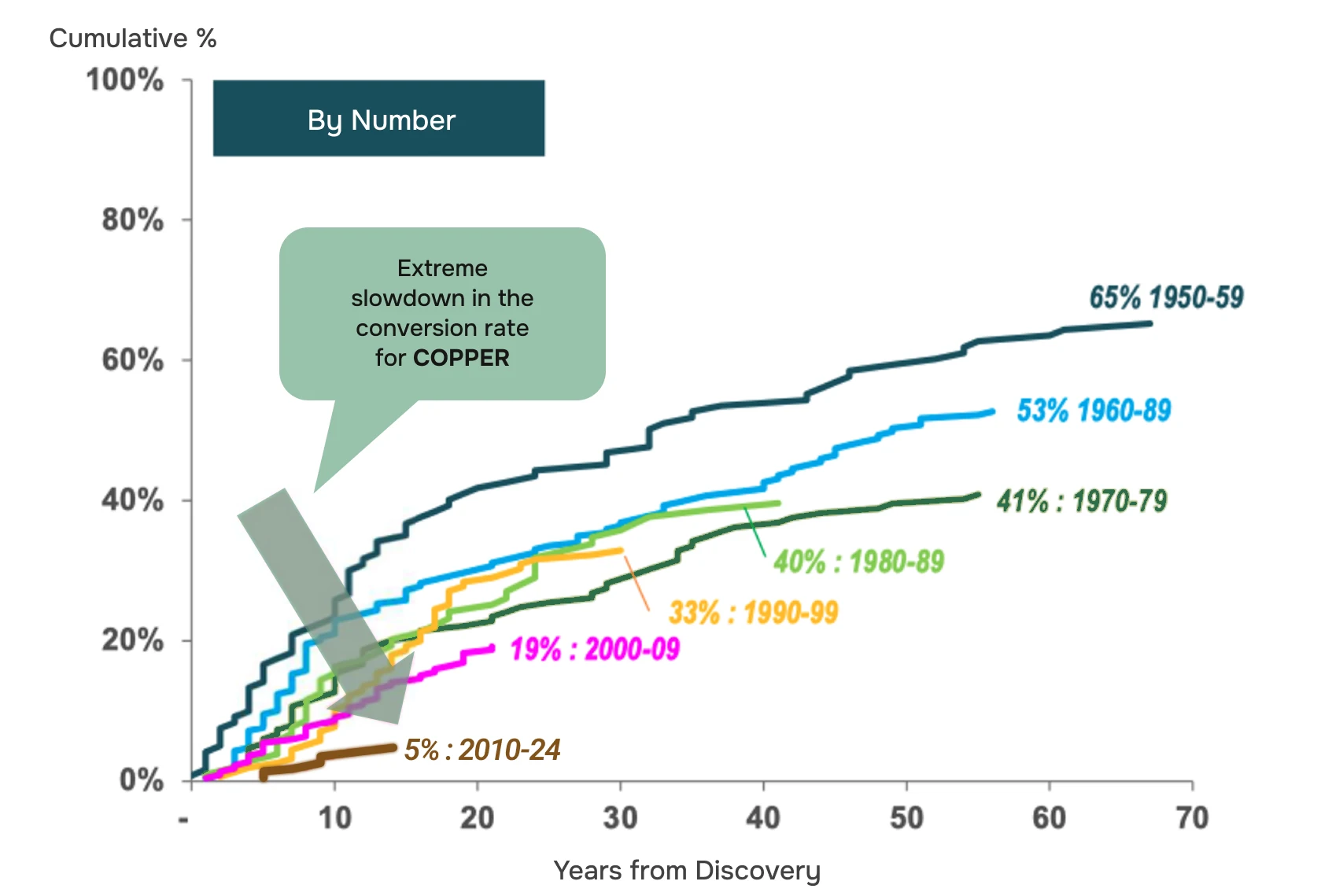

But even rare successful discoveries don’t solve the time problem. Historically, the path from discovery to production startup has been shorter. In the mid-twentieth century, a significant portion of discovered fields transitioned to commercial development within 15-20 years. Today, the process is noticeably longer and more complex.

On average, about 17 years now elapse between the time of discovery and the start of production. At the same time, a smaller proportion of sites reach the mine stage than before. In other words, the situation is twofold: we are finding fewer new deposits and it is taking longer to bring those that we do manage to discover into production.

Against the background of demand forecasts, this is becoming critical. According to various estimates, by the end of the 21st century, global demand for copper could reach 50-65 million tons per year. To get close to the Net Zero targets by 2050, the world, according to a number of researchers, will need, in the order of 200 new large-scale copper mines. Given the current pace of exploration, approvals and commissioning, such a scale does not just look challenging – it looks structurally unattainable within the current industry development model.

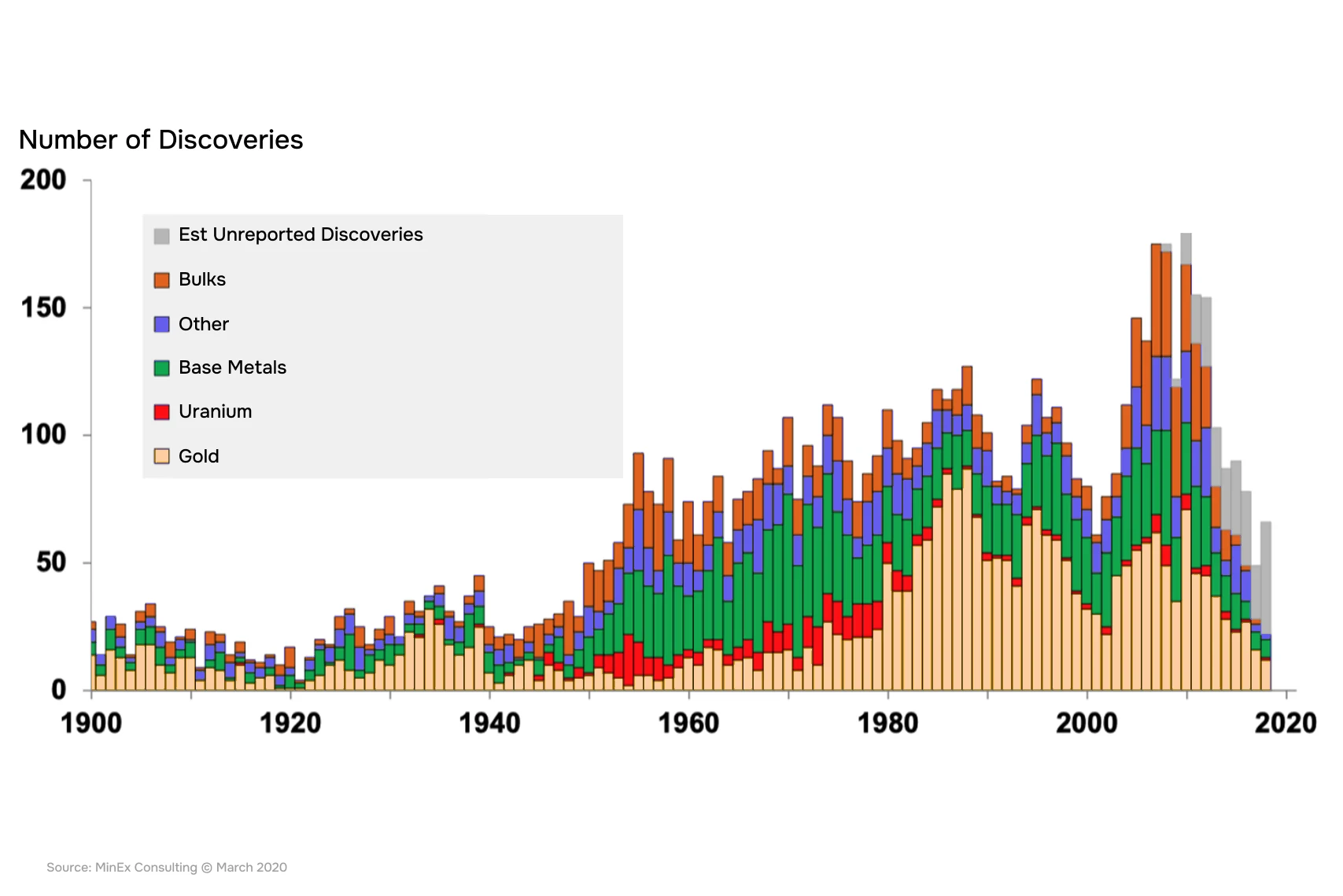

The situation is exacerbated by a steady decline in discovery rates. This is not only true for copper, but also for gold, base metals and uranium: in all cases, the discovery curves are going down. We are no longer finding deposits on the scale that characterized the 20th century.

Deeper, more complex and riskier: how the search space has changed

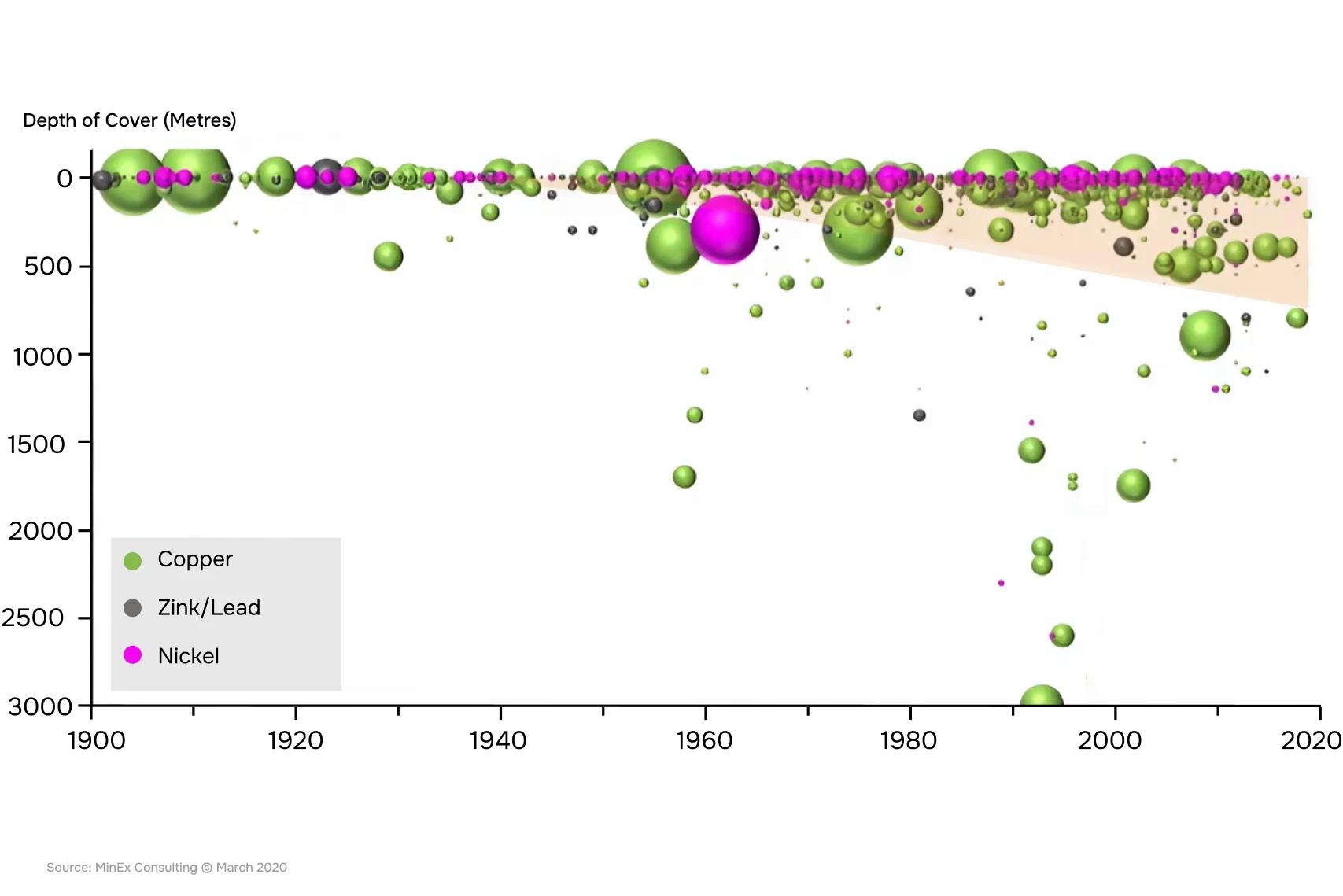

The search space itself is also changing. Before the 1980s, large deposits were usually found near the surface or at shallow depths. Since the 2000s, the situation has been fundamentally different: new targets are deeper, smaller and have complex geometries. Today, exploration is increasingly focused on depths of 500-1,000 meters and more, while there are few large, accessible and easily discoverable deposits left.

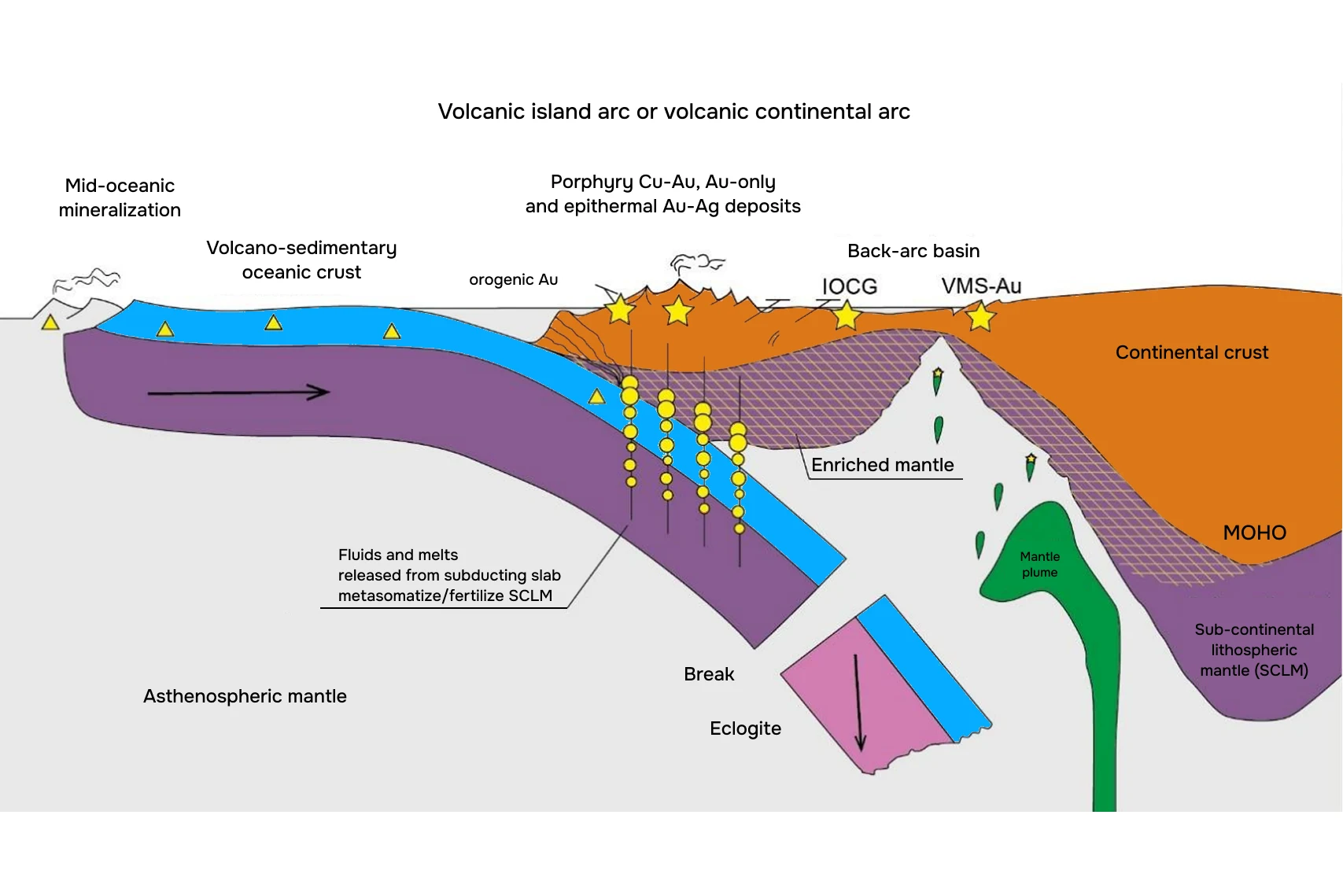

Ore deposits do not occur by chance. They form under strictly defined geodynamic conditions related to the Earth’s tectonic evolution. This is why modern geology generally has a good understanding of where it makes sense to look for ore.

Virtually all major world-class deposits are confined to zones of deep geophysical and geochemical anomalies in the lower crust and upper mantle. These may be subduction zones and volcanic arcs, back-arc basins, craton margins, or regions affected by mantle plumes.

For example, porphyry copper-gold deposits and epithermal systems are characteristic of volcanic arcs, VMS deposits are characteristic of volcanic-sedimentary complexes of oceanic crust, and IOCG systems are characteristic of zones of interaction between enriched mantle and continental lithosphere.

The key point here is that all these deposits are “tied” to deep processes. Fluids and melts released from subducting plates or rising from the mantle metasomatize and “fertilize” the lithosphere, creating conditions for the subsequent concentration of metals. This is why large ore systems are almost always deeply rooted in the lower crust and mantle, even if the mining itself takes place much higher up.

This leaves a fundamental limitation: we have a much better understanding of modern and relatively “young” tectonic settings than we do of early Earth conditions. For the Archean time (more than 3 billion years ago), the nature of tectonics is still a subject of scientific debate, which directly affects the interpretation of ancient ore systems. And it is in these ancient cratonic regions that much of the world’s metal reserves are concentrated.

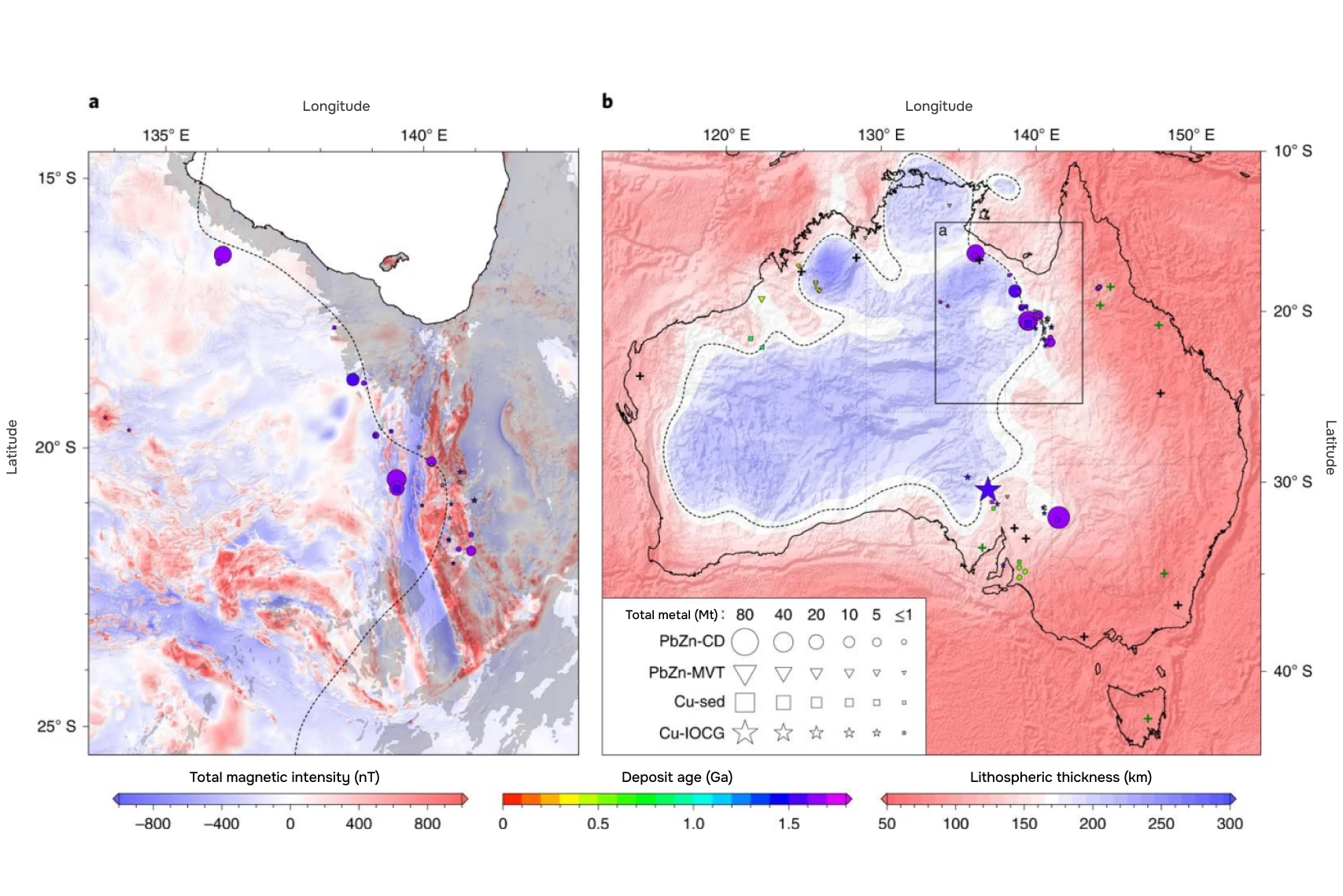

An illustrative example is Australia’s IOCG deposits, which are systematically confined to the edges of cratons. It is in these zones that the lithospheric structure allows deep ore-bearing fluids to rise upward and form large-scale mineralization zones.

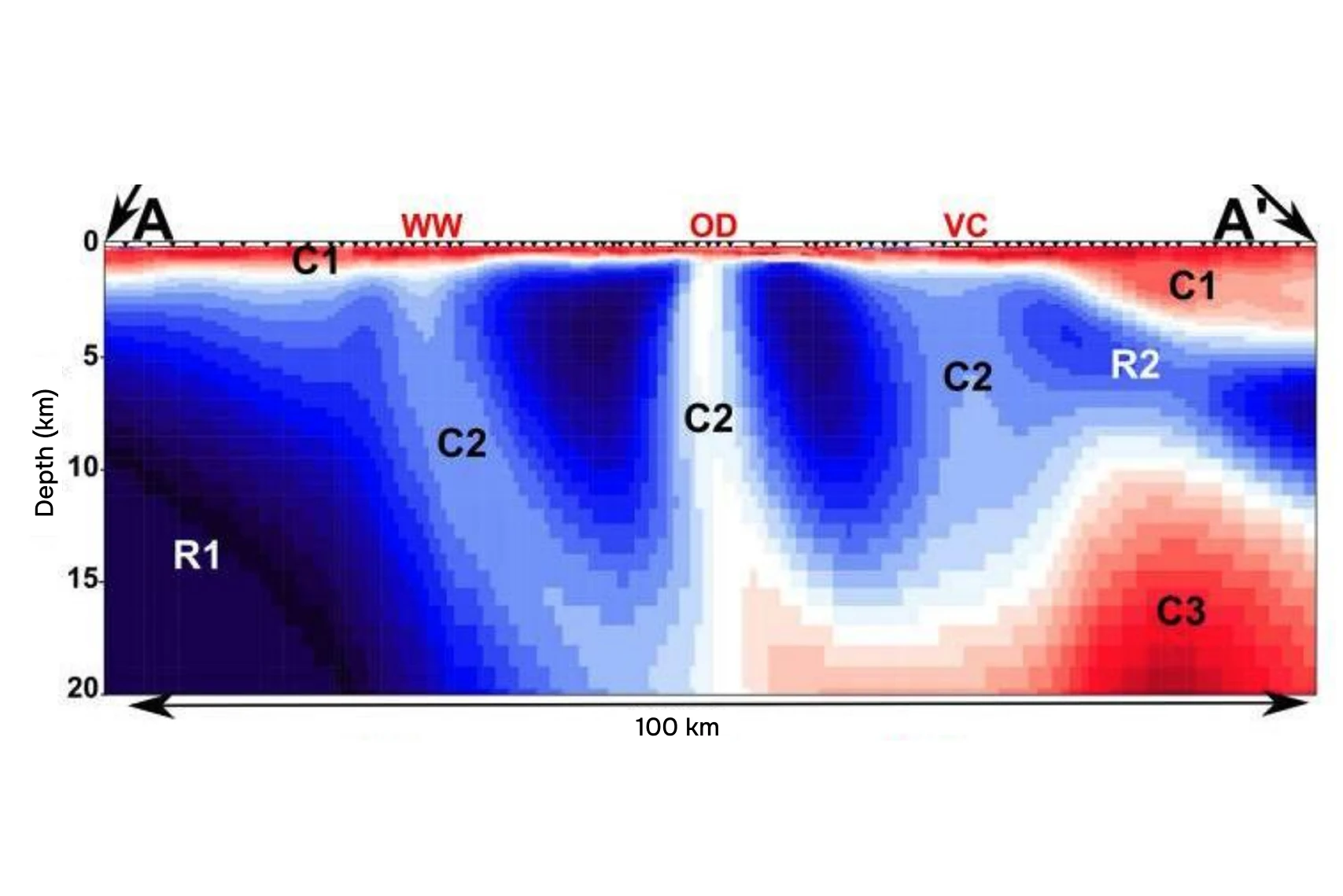

From this, a working model of exploration is built: identify the craton → define its boundaries → focus prospecting along its edges. Deep geophysical data confirms the effectiveness of this approach. Geoelectric models, including profiles over the Olympic Dam deposit, show extended conductive zones in the crust and upper mantle associated with both active mines and prospective zones of mineralization.

Thus, the problem is not just geology as a science. Increasingly, the scale and organization of exploration are becoming decisive: the availability of regional depth models, long-term funding and a strategic vision for reserve growth. Against this background, it is particularly revealing to look at how different countries are responding to the challenge of resource depletion.

Some are building long-term national geological mapping and exploration programs, while others are losing ground despite their high natural potential. In the following, it makes sense to look at specific examples and compare how China, Australia and Canada are coping with this task.

China: geology as a national strategy

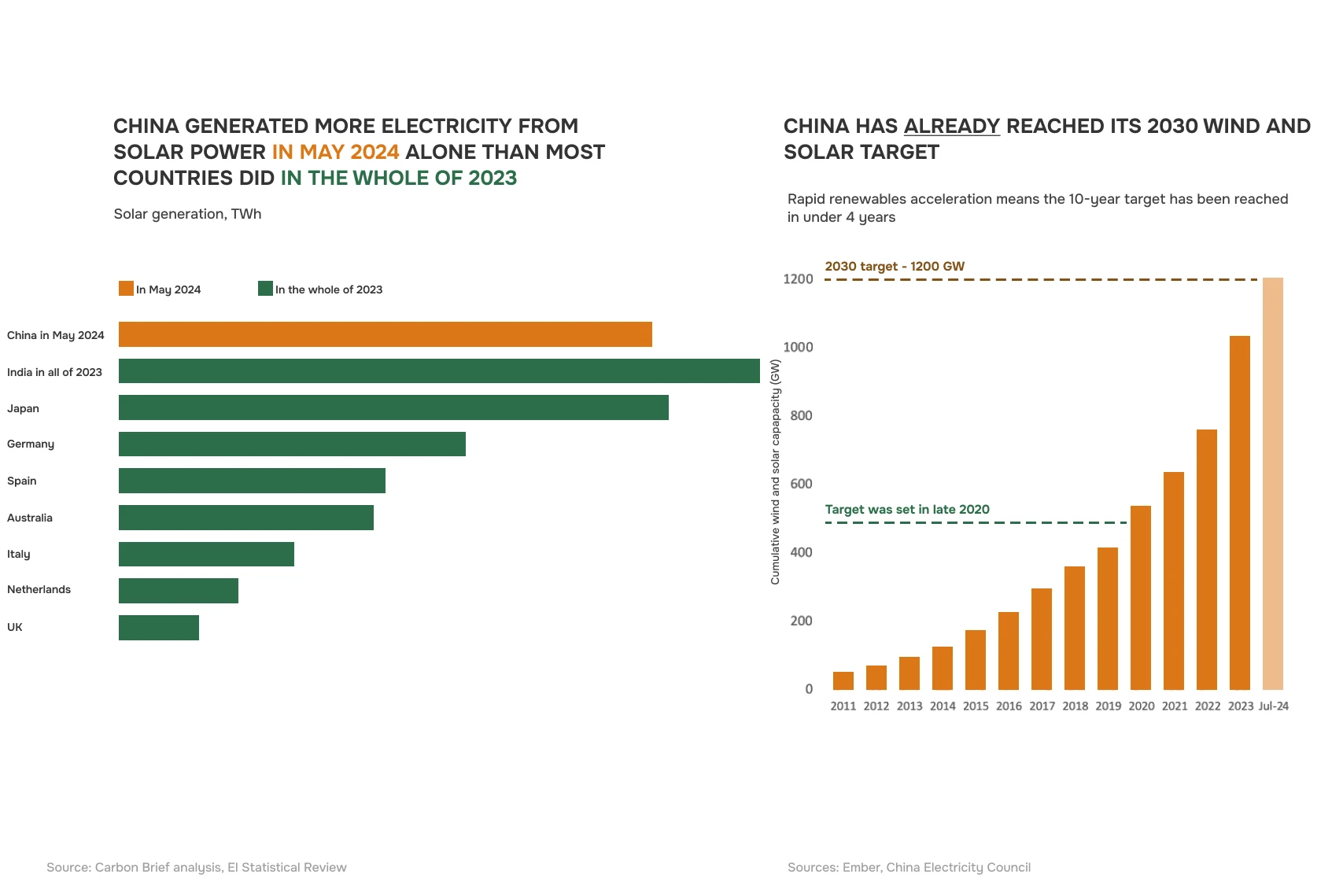

Against the backdrop of global climate declarations, China remains one of the few countries that are preparing for the energy transition not by slogans, but by controlling its material basis. Already by mid-2023, the country has exceeded the target of 1.2 TW of installed wind and solar generation capacity formally set for 2030. But the key part of the strategy lies not in energy, but in raw materials: in parallel, China is systematically building control over critical metals, without which the transition itself is impossible.

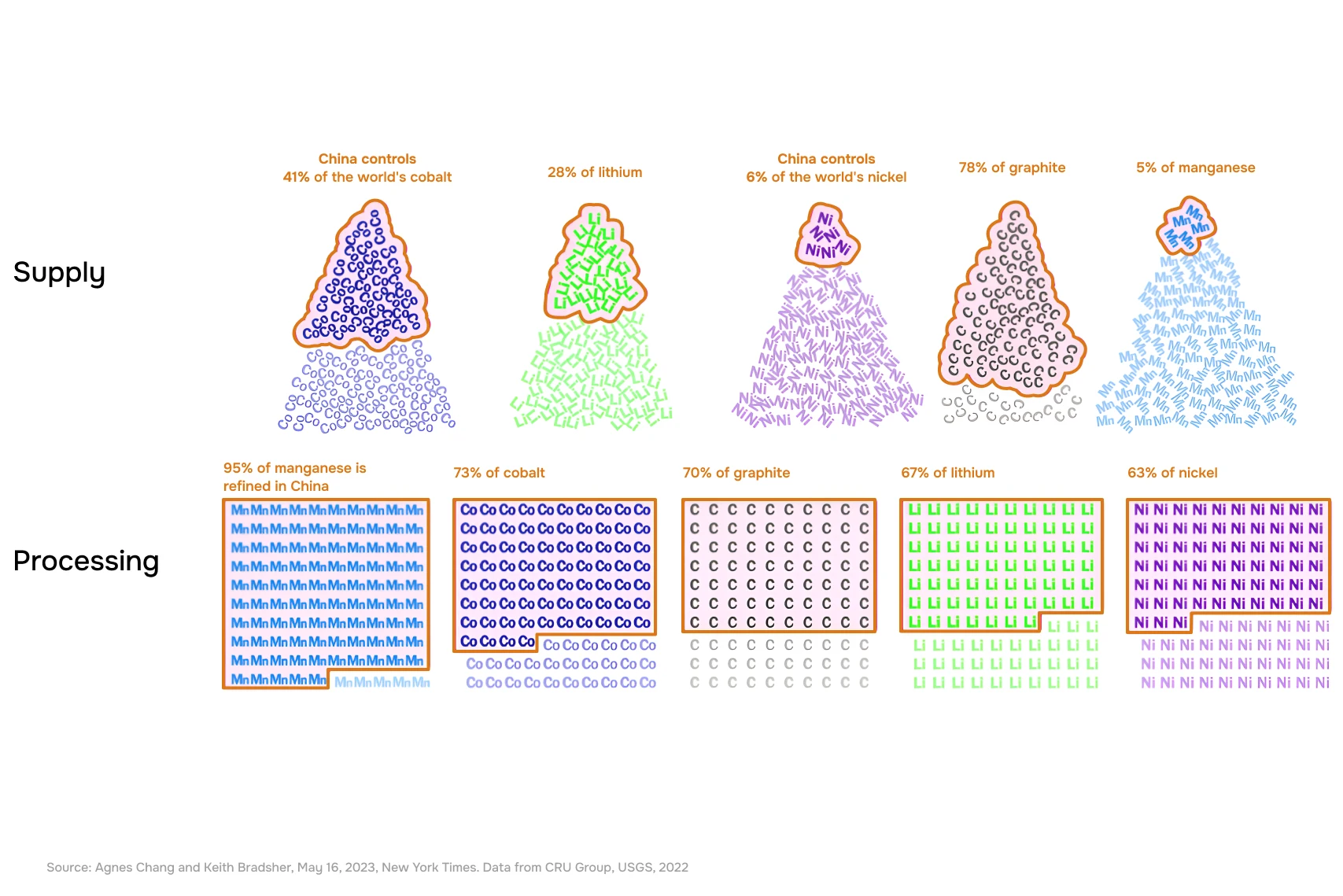

In recent years, export restrictions have been imposed on gallium, germanium, graphite and antimony – steps that make it clear: access to materials is no longer considered solely a market issue. China may not dominate the extraction of all critical elements, but it holds key positions at the downstream stage, where the real dependence of the global economy is formed. As a result, it is not individual companies but entire national green transition strategies that are vulnerable if they do not have their own resource base behind them.

This is why China is investing in geology as an element of strategic sovereignty. The national SinoProbe program is not an academic project, but a decision-making infrastructure aimed at understanding the deep structure of the lithosphere and the potential of new ore systems. At the same time, the country is increasing its control over foreign mining assets based on a simple logic: the energy transition is impossible without new deposits, and geology is not an annex to climate policy, but its foundation.

Australia: deep geology as a national project

Australia is acting pragmatically and consistently in this situation. The resource and energy sector remains the foundation of its economy: minerals and energy account for about two thirds of the country’s export earnings. In such conditions, the key task is not to develop individual areas, but to understand the structure of its own lithosphere on a continent-wide scale.

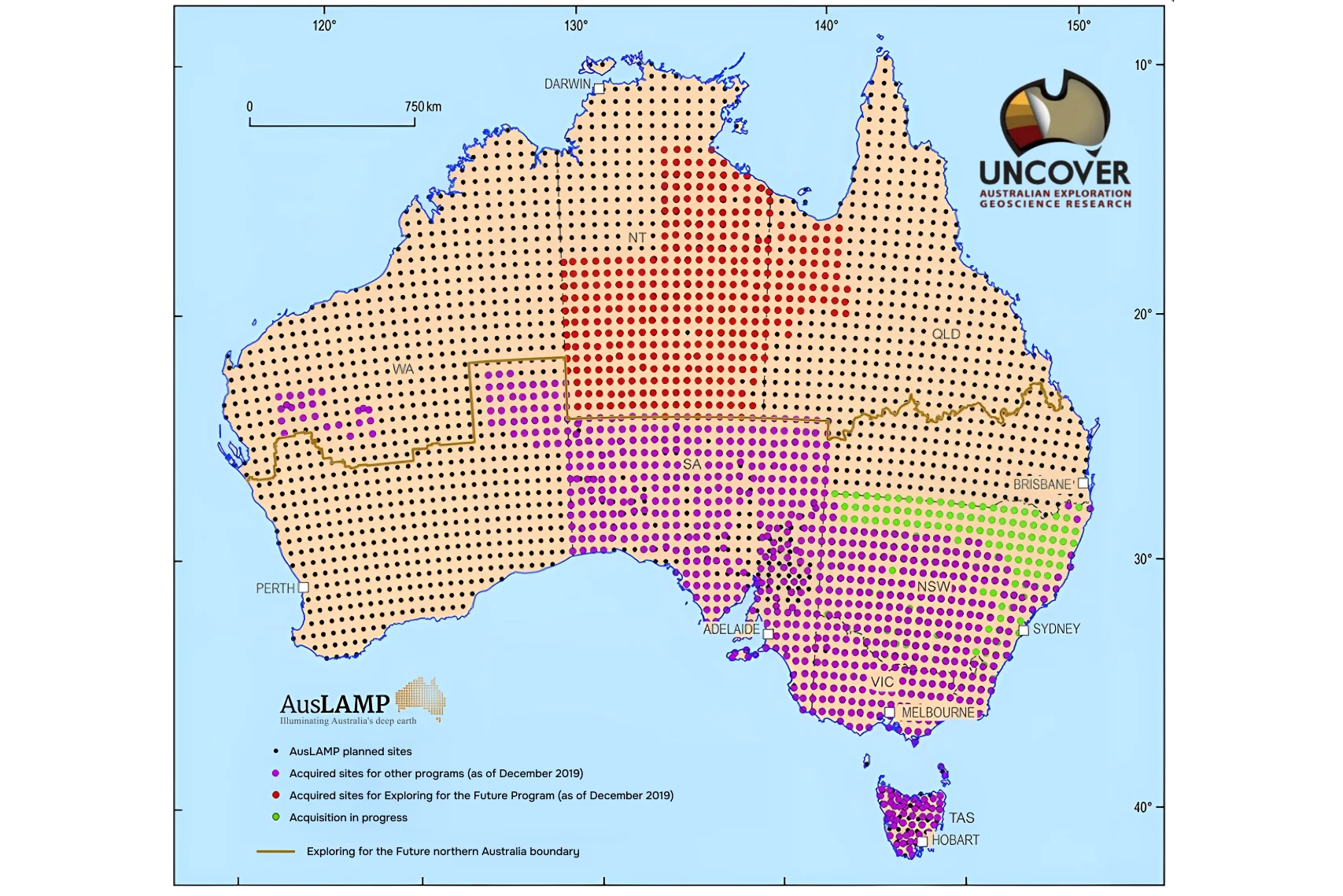

It is in this logic that the program was launched in Australia Uncoverprogram, aimed at finding deposits hidden beneath the thick sedimentary cover. It is part of a broader government initiative, Exploring for the Future, which integrates regional geoscience research into a single national system. It includes large-scale magnetotelluric networks (including the AusLAMP program), regional aeromagnetic and electrical surveys, and seismic studies. All these data are linked into deep models of crustal and lithospheric structure.

As interpreted by Alan Jones, the Australian approach shows what a modern strategy for building up a mineral base might look like: first, a systematic regional understanding of the deep structure of the territory, then a targeted search in the most promising zones, and only then local exploration. It is this order of operations that allows us to work with the type of deposits that are becoming the norm today: deeper, more complex and less obvious than the targets of the last century.

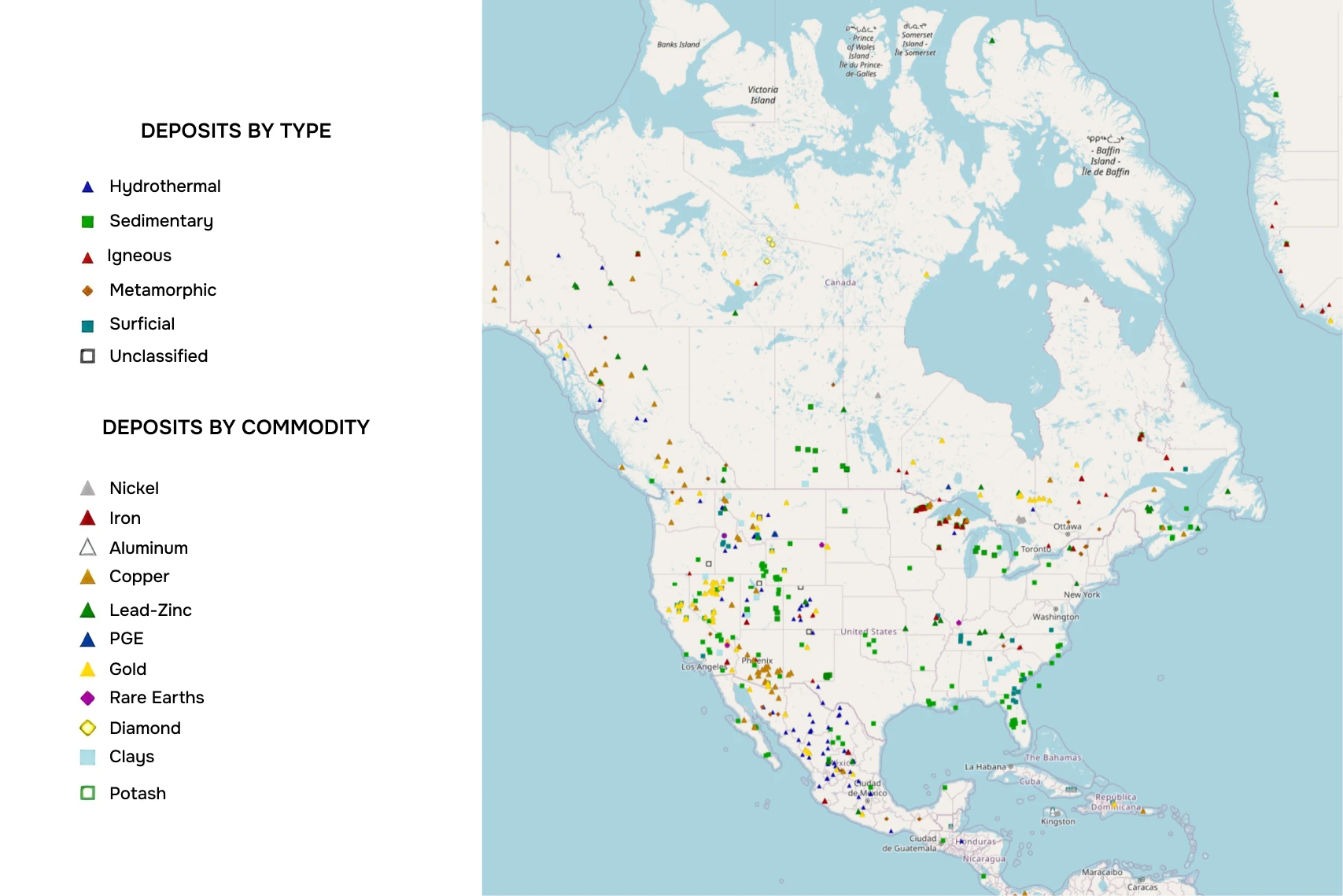

Canada: potential is there – strategy is lacking

Canada is often heard talking about critical minerals, and for good reason: the country is really rich in “battery” and infrastructure metals (nickel, cobalt, graphite, lithium, etc.) – and has formalized this in its own Critical Minerals Strategy. But the problem that Alan Jones points out is not that “there are no metals”, but that the national raw materials agenda and geological “picture of the country” have not yet been assembled into a single, long-term plan: what we are mapping, where we are looking for, what chains we are building, what projects we are bringing to mining and processing – and who is responsible for it.

The second part of the paradox is the loss of “national champions”: the largest historical Canadian players in metals ended up being controlled by global corporations. For example, Inco was taken over by Vale in 2006. And around Falconbridge in 2006, there was a major deal to buy Xstrata (Xstrata later became part of Glencore).In Jones’s logic, this means: even with strong geology, a country risks remaining a “resource jurisdiction” (i.e., a territory where there are metals in the ground, but decisions about exploration, development, investment and supply chains are made externally – by global corporations and markets, not by the state itself), and with limited influence over how and why those resources are used.

Hence, his prescription for Canada sounds rigid and simple: less point initiatives, more unified architecture. That is: a nationwide regional mapping program (including in-depth methods), a long-term plan for priority metals and projects, and a “exploration → infrastructure → processing → ethical supply chain” linkage. Otherwise, talk of leadership in critical minerals will remain a beautiful declaration – even though Canada does have a window of opportunity.

Ethical extraction and social license

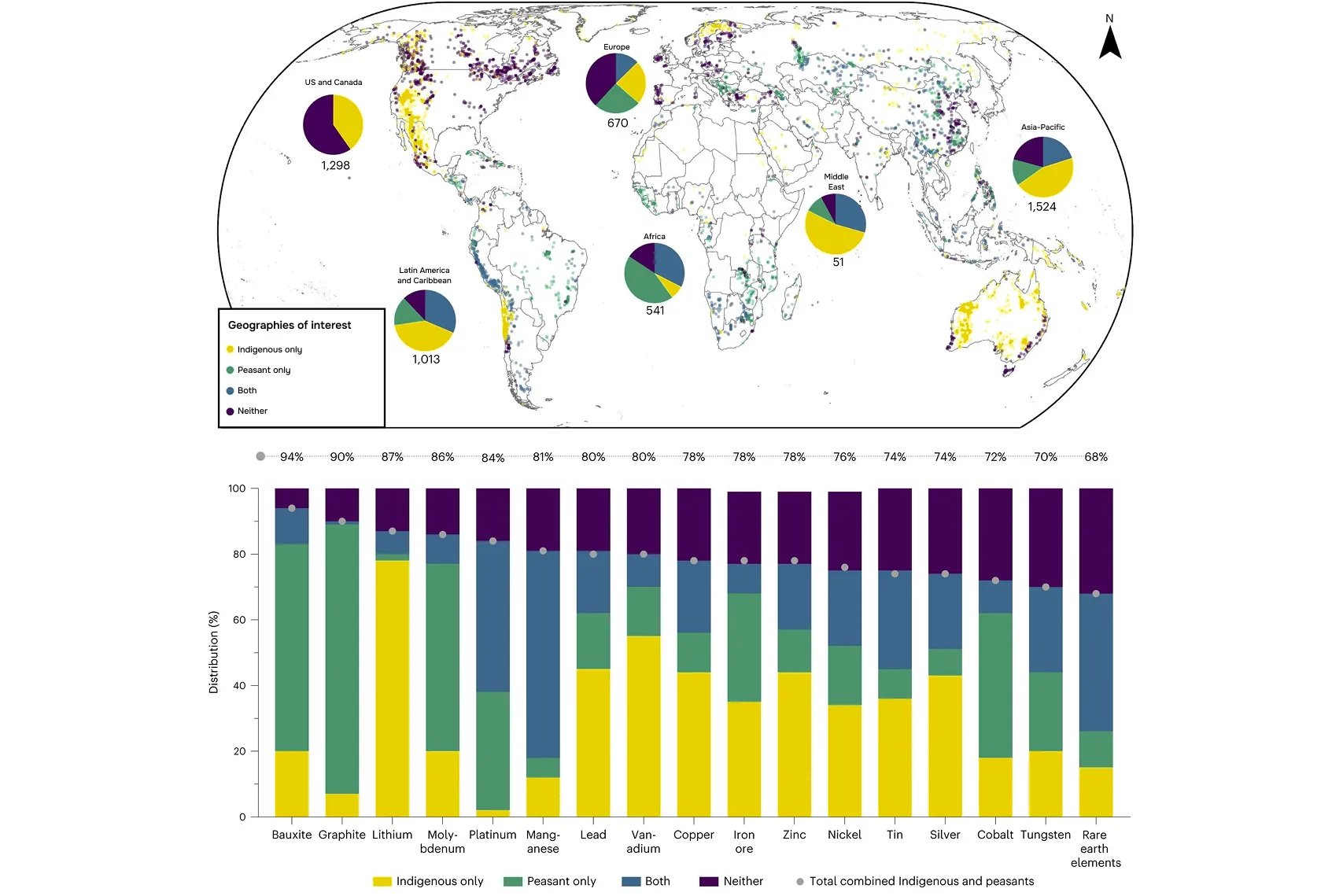

One of the key constraints to the energy transition is the social license to mine. A study published in Nature Sustainability in 2022 found that 54% of prospective mining projects are located on indigenous lands. This means that it is no longer possible to scale up mining according to the old model – without taking into account the interests of local communities – and these projects face protests, lawsuits and often never come to fruition.

In response, governments and businesses have begun to build mechanisms to control supply chains. The EU, for example, has introduced requirements for traceability of the origin of certain metals in order to eliminate the financing of conflicts. In parallel, industry initiatives are developing – Responsible Minerals Initiative, Responsible Cobalt Initiative and similar programs for copper, tin and other metals. International practice increasingly speaks not just of “green energy”, but of ethical energy, i.e. an energy transition that takes into account not only CO₂ emissions, but also the origin of metals, the conditions of their extraction and their impact on communities. This approach is enshrined in OECD, IEA and UN documents and is becoming part of real regulatory policy.

A separate level of risk is associated with cobalt. Much of the world’s production is concentrated in the southern Democratic Republic of Congo, where artisanal mining, child labor and opaque supply chains are common. This poses not only humanitarian challenges, but also systemic risks to the entire energy transition: dependence on a single region with high social instability makes supply vulnerable and politically sensitive.

From the Editor. It is important to understand that the requirements for social license and the rights of indigenous peoples today are most strictly formulated in the countries of the USA, Canada, Australia and the EU. There, the extractive industry operates under strong social and legal pressure, and projects without the consent of local communities are almost guaranteed to be blocked. In other regions of the world, such restrictions are weaker, and this is where unethical mining is increasingly shifting. As a result, some countries formally “clean up” their supply chains, while the real environmental and humanitarian costs are shifted to others. Therefore, the issue of ethical mining is not a local Western agenda, but a global factor in the sustainability of the supply of critical metals.

Supply risks: when dependency becomes critical

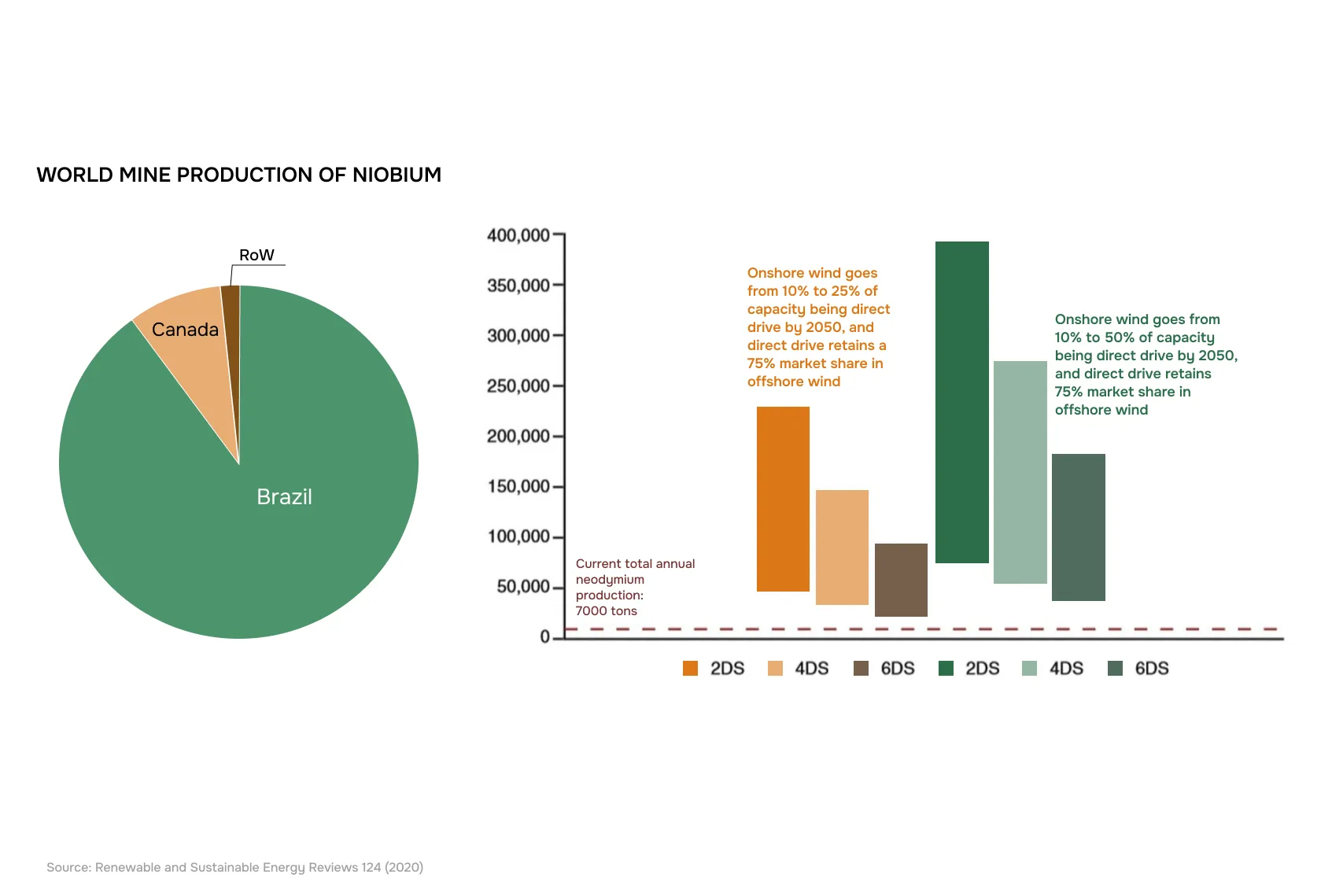

But beyond ethics, there is another fundamental challenge – concentration of production and vulnerability of supply. One of the most obvious examples is niobium. More than 90% of the world’s production of this metal comes from a single deposit in one country – Brazil. Niobium is used in stainless steel, aircraft engines, building structures, magnets and medical equipment.

One key example is neodymium, needed for onshore and offshore wind turbines. Today, global production is about 7,000 tons per year. However,for the scenario of keeping warming below 2 °C, the need for neodymium exceeds the current supply by a factor oftwo.

It is enough to imagine a political decision to restrict exports – and a significant part of the world industry will be in a vulnerable position. Canada is the second largest producer of niobium, but its share is not comparable to Brazil’s.

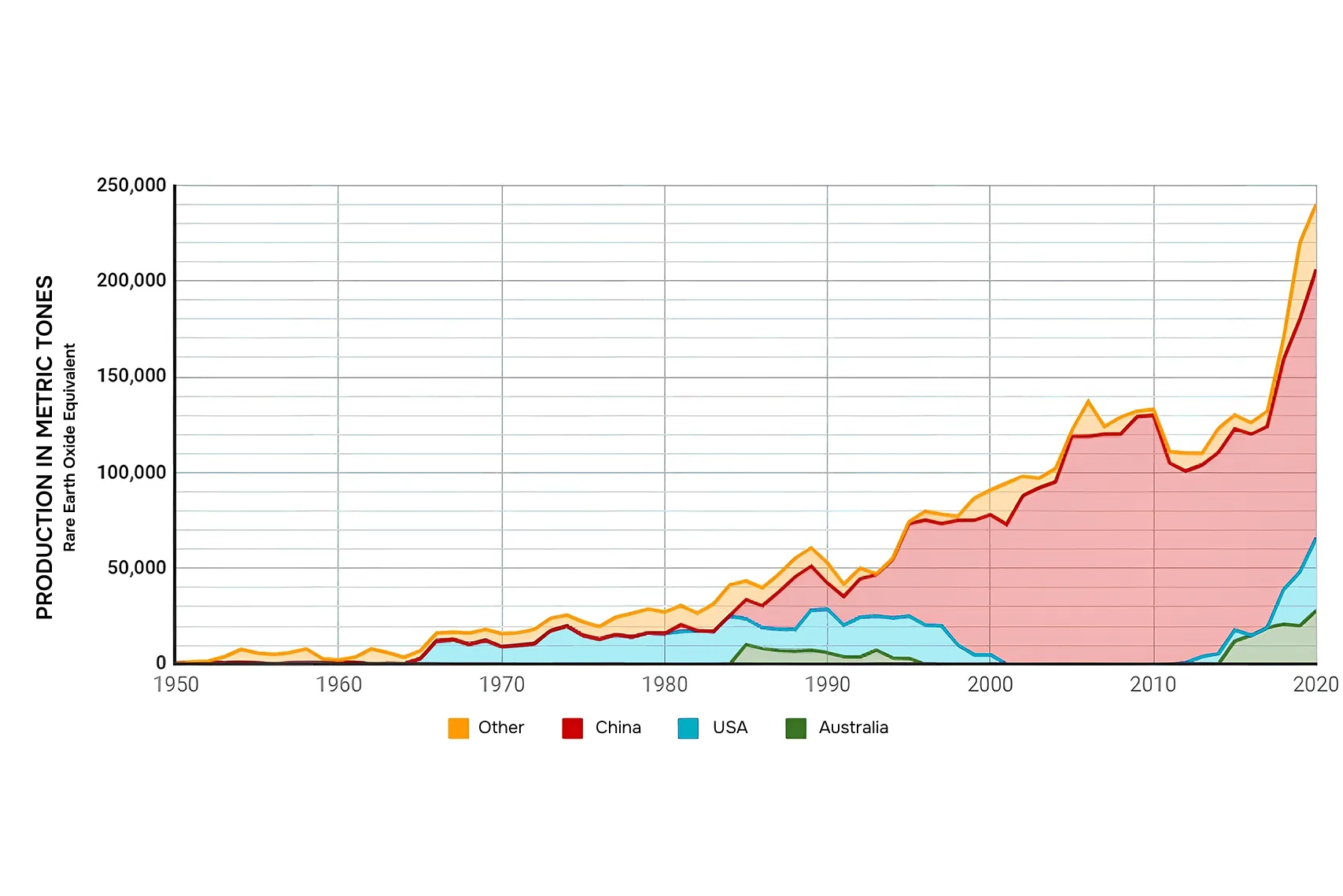

A similar situation has already happened with rare earth elements. Until the mid-1980s, Australia and the United States were their main producers. Then China entered the market, and the rest of the world lost its own supply chains for years. Between the early 2000s and around 2015, China effectively became a near-monopoly supplier of REEs. It was only after that that the US and Australia began to urgently restore their own production.

Who will ensure the energy transition

Alan Jones talks about his profession without illusions, but also without disappointment. He says he has had a “wonderful career in geophysics” and would be willing to go down that road again. Today, however, geoscientists face a systemic problem: the profession is rapidly aging.

At the same time, geosciences remain one of the most stable and prosperous fields in terms of working conditions:

- the unemployment rate here is extremely low;

- incomes are high – median salaries for professionals exceed $100,000 per year;

- relative gender equality is maintained, which is rare in technical disciplines.

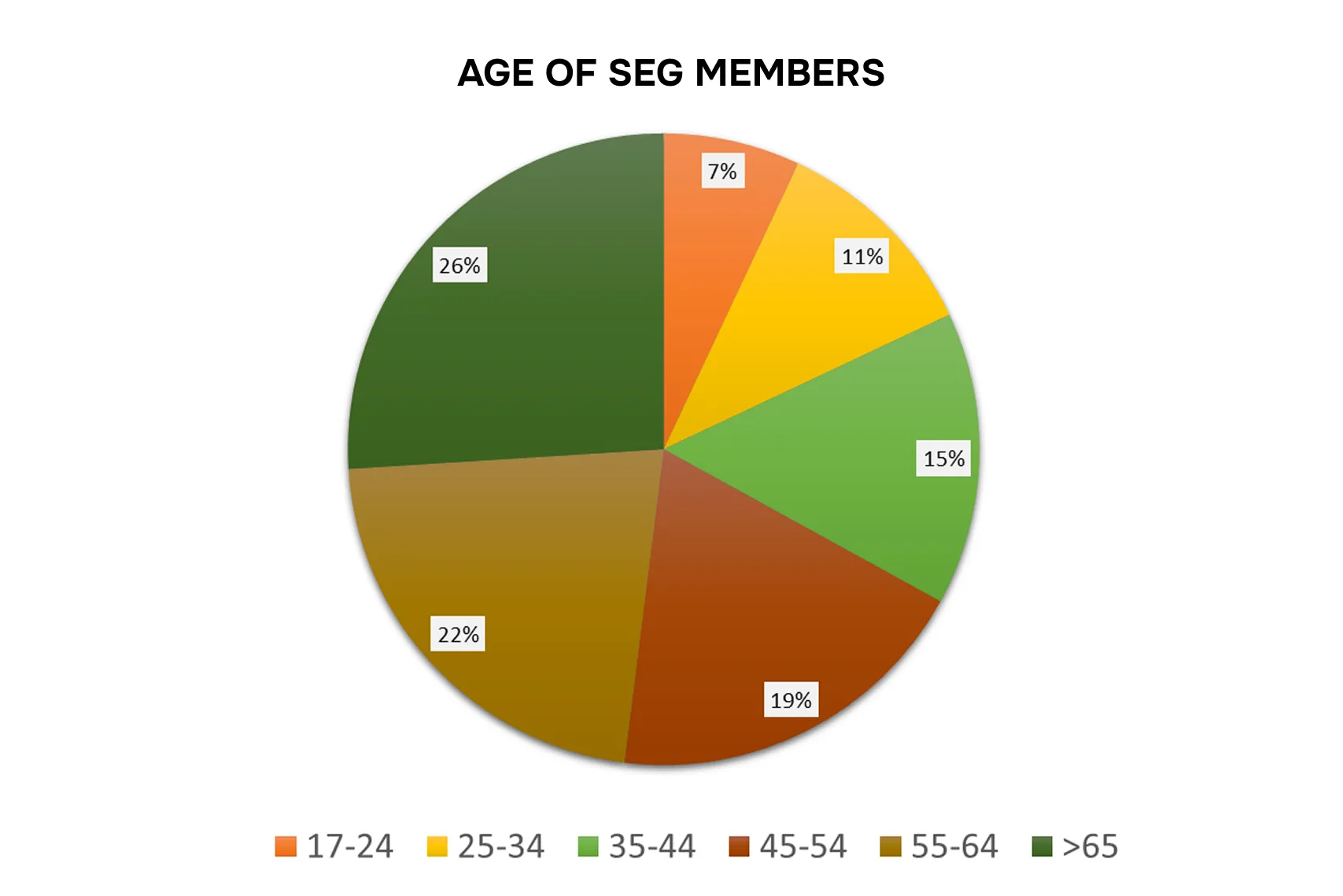

But the demographic picture looks alarming. According to the Society of Exploration Geophysicists (SEG), nearly half of active professionals are over 55, while the 23-34 and 35-44 age groups are minimally represented. This means that in the coming years the industry will face a mass retirement of specialists – and with them the decades of practical experience accumulated.

In parallel, the inflow of young personnel is falling. Data published in 2021 in the journal EOS (AGU) show that the enrollment of students in geological and geophysical specialties in the USA, UK and Australia has decreased by about two-thirds compared to the peak values of 2013-2014. The American Geosciences Institute (American Geosciences Institute) estimates a possible shortage of about 130,000 professionals in the US by 2030. At the same time, only about 25,500 new graduates will enter the profession, while a significant proportion of current professionals will retire.

This is where the question “is it worth going into geology today” ceases to be rhetorical. In terms of long-term demand, geosciences will be needed more than ever. But without systemic support for education and training, the risk is that there will be no one to realize the energy transition.

Metals and people: the foundation of the energy transition

The energy transition, the growth of electricity consumption and digital technologies are no longer a forecast, but a reality. Wind and solar power plants, electric cars, new power grids, data centers, servers for artificial intelligence, billions of smartphones and laptops – all this requires a material base. Metals. Lots of metals.

The calculations in the article show that even with maximum recycling, the world will face shortages of copper, lithium, cobalt and other critical elements in the coming decades. These materials do not appear out of thin air and cannot be “assigned” by political decision. They must be found in the ground, evaluated, and exploited on a scale never before experienced by mankind.

This is where the energy transition is caught up in a complex societal conflict. Much of the negative attitude towards mining is due to its heavy historical legacy: pollution of water, soil and ecosystems, and examples of irresponsible mining. These histories are well known and still shape public perceptions of the industry.

However, this does not imply a rejection of mining as such. Society has changed, and today in most countries it is no longer possible to mine in the same way that was done 50 or 100 years ago – ‘at any cost’. On the contrary, there is an emerging demand for ethical mining, with environmental standards, transparent supply chains and respect for the rights of people and communities. But even with the most stringent requirements, the basic fact remains: without metal mining, the energy transition is physically impossible.

And then the conversation inevitably turns to the level of the profession. If today it seems that geology and geophysics are not the most obvious areas for the future, the figures say otherwise. As the demand for metals grows, it is specialists who can find, understand and responsibly develop the subsurface that will play a key role. Everyone needs metals. They need to be found. And someone has to do it.

So if you or your children have a question about whether to go into geology, after all these facts and figures, the answer is probably already obvious.