The global mining industry is experiencing a structural shift. Investments in geological exploration are being reduced from scratch, and money is increasingly being directed to expand existing enterprises. This is confirmed by data from recent years: the production of many metals continues to grow, but new mines are opened less and less often. The paradox can be explained simply – companies prefer to invest where they already operate.

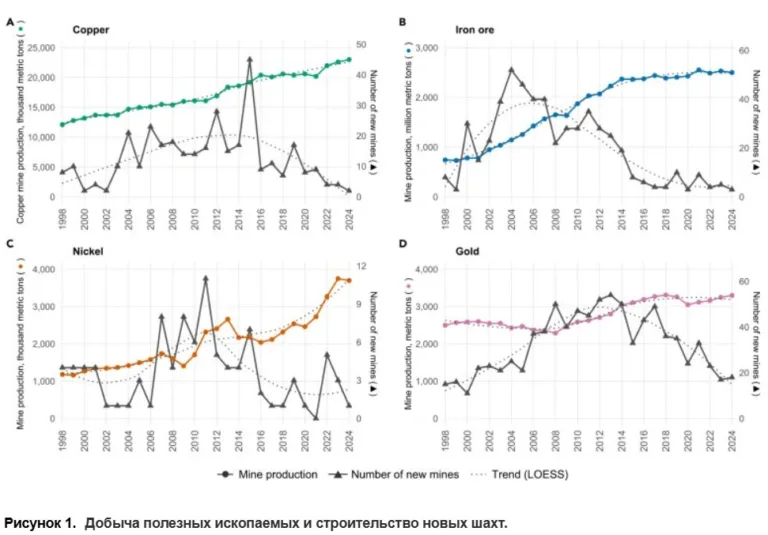

The peak of commissioning of new copper mines occurred in 2015. For iron ore this is the early 2000s, for nickel – 2010-2012, for gold – 2012-2014. After these peaks, the number of new projects began to decline, but production volumes did not fall, but increased. This means that old enterprises are being developed. Companies are expanding their quarries, modernizing factories, and extending their service life.

The trend is especially noticeable in copper, iron ore and nickel. There, production is increasingly concentrated on large, long-running assets. For gold, the picture is a little blurry due to the fragmented nature of the industry and the short life cycle of mines. Lithium is still out of the ordinary. Its role in the energy transition has changed the structure of demand, and the market is not yet settled.

Recycling and reuse are not a solution yet. Recycled copper accounts for less than a fifth of global supply, and recycled lithium accounts for about 1%. So the main increase comes from existing deposits.

The redistribution of capital is clearly visible in the structure of investments in geological exploration. Large companies are spending less and less on searching for new deposits. According to the S&P Global classification, exploration is divided into three stages: initial (search from scratch), late (feasibility study) and near-mine (additional exploration in existing areas).

Total exploration spending has fluctuated since 2010, peaking in 2012, then falling by 2016 and stabilizing at about $6 billion a year. But the structure has changed dramatically. In 2024, almost 60% of all investments went to near-mine exploration. Since 2016, this segment has grown by 130%. Investments in the early and late stages are only about 20% each and are practically not growing in absolute numbers.

This means that companies consciously avoid risks associated with searching for new deposits world level. Such discoveries are becoming rare. Instead, they prefer to develop sites with ready-made infrastructure, where financial and regulatory risks are lower, and there is less likelihood of social resistance.

Thus, the industry is conserving its raw material base around existing assets. This gives stability here and now, but creates risks for the future. Sooner or later, reserves will run out, and there may not be new large deposits ready to replace them.

Source: @Metals_Mining

Image: S&P Global