Diamonds have always seemed a symbol of strength and stability – but today even this industry is bursting at the seams. The deposits are being depleted: Canada will lose three large pipes in the coming years. The market is flooded with synthetic stones: they are cheaper, cleaner, and only a specialist can distinguish them from natural ones. Russia, one of the largest producers, faces sanctions that hit exports and technology. ALROSA, which holds up to a third of the world market, is losing sales and is forced to shut down unprofitable areas.

What’s going on with diamonds? Why did an industry that seemed eternal come under pressure? And can artificial crystals really replace natural ones? We are looking into this together with Vladimir Sergeevich Shchukin, a geologist who has been studying for more than 50 years searching for diamonds. He discovered kimberlite pipes in Canada, participated in the development of deposits in the Arkhangelsk region, including the Grib pipe, and saw from his own experience how the world market was changing. Today it helps to understand: do natural diamonds still have a future – and what kind?

Where are diamonds mined: the world’s main players

To understand what is happening with the diamond industry today, let’s look at where mining continues in the world and which countries hold positions in the market.

Russia: leader under sanctions

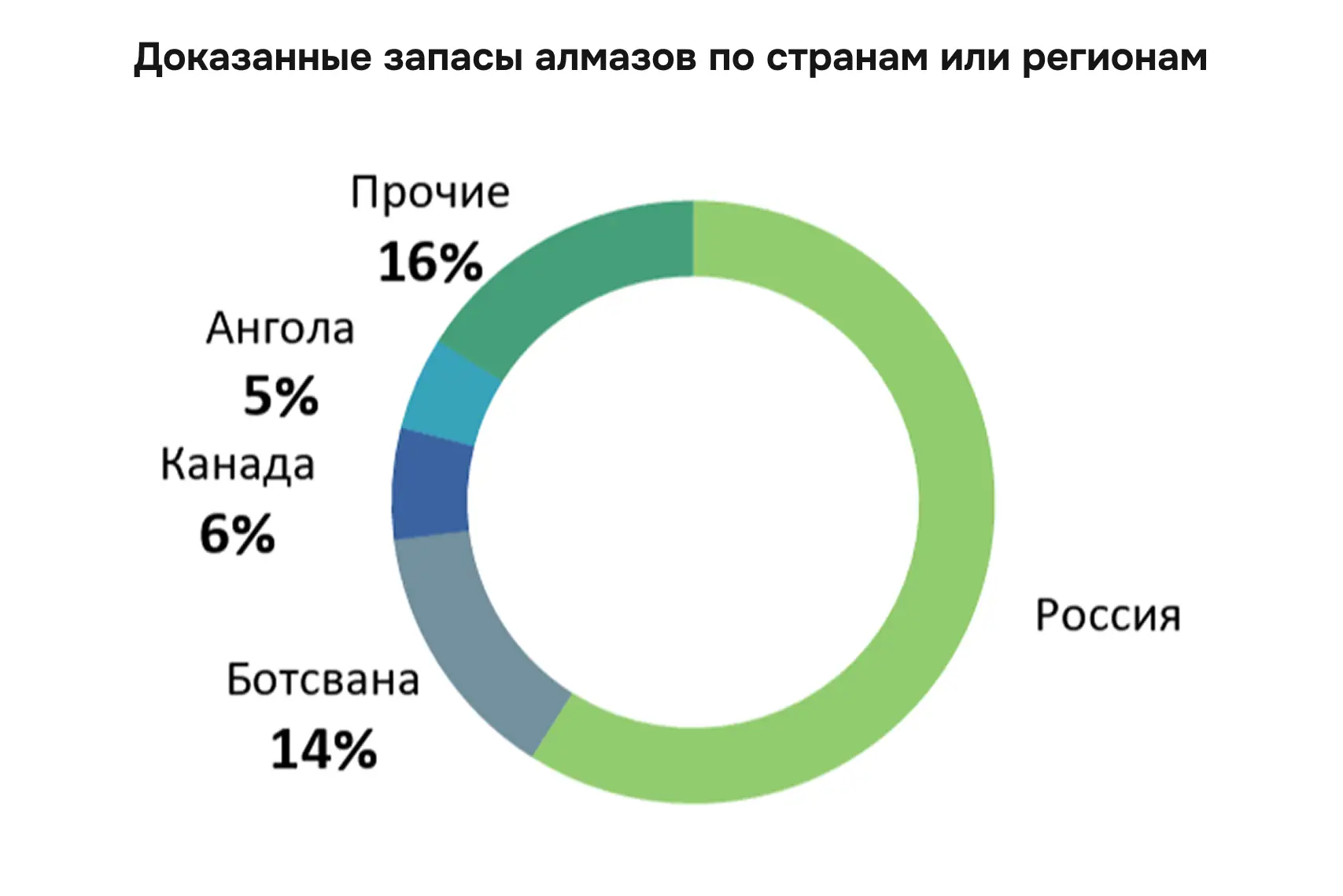

Russia remains the largest player in the global diamond market: about 30% of all production comes from ALROSA. The company works in Yakutia And Arkhangelsk region, controls dozens of pipes, as well as the largest placer deposit. But since 2022, the situation has changed: sanctions have closed the usual export channels, including through Angola, and limited access to equipment and technologies.

This forced ALROSA to suspend production in unprofitable areas and rely on import substitution. In parallel, the company is developing the Mir Glubokiy project – a new underground shaft that will allow the flooded Mir field to be returned to operation. In 2024, the project passed the examination.

Despite the difficulties, Russia still has a unique advantage – the world’s largest proven diamond reserves. Geologists believe: if we manage to develop exploration and develop new tubes, the country can not only maintain its position, but also again become a source of growth for the entire industry.

Africa: wealth and challenges

Africa is the historical center of world diamond mining. It was here that the industrial history of diamonds began in the 19th century, when the first kimberlite pipes were discovered in Kimberley (South Africa). Since then, the region has remained one of the main suppliers of raw materials.

Today the leaders are Botswana, Angola and Namibia. The largest pipes in Botswana are Jwaneng and Orapa, which manages Debswana is a joint venture between De Beers and the country’s government. They account for a significant portion of De Beers’ supplies. In Angola continues work at the Katok pipe, where ALROSA participated until 2022, but due to sanctions, the project came under the control of Middle Eastern investors. And in Namibia, mining is carried out by Namdeb, a partnership between De Beers and the local government.

According to Vladimir Shchukin, who visited one of the mines in Namibia, the potential of African deposits remains high. This is due to two key factors: well-developed geology, which allows production to be planned for decades to come, and the active participation of states – through equity partnerships in projects, investor support and infrastructure development. This combination makes Africa an attractive region even in times of global crisis.

Canada: from blind discovery to loss of mines

If Africa is the story of a century of mining, then Canada is the youngest country where productive kimberlite pipes were discovered. The first large deposits were found here only in the 1990s, and Vladimir Shchukin became one of the discoverers.

He recalls:

“There weren’t even materials there. Clean card. I just found a structure on it that I thought was promising. I arrived by helicopter and after 50 meters I found the phone. That’s how work began in the area.”

These discoveries became the basis of the Canadian diamond industry. However, the country is now experiencing a recession: after 2025 are closing three fields at once – Gacho-Quey, Diavik and Ekati. This calls into question Canada’s continued role as a supplier to the American market and highlights how rapidly both the rise and fall of the industry can be.

Regions where the Diamond Age has already ended

Australia has been an important player in the diamond market, primarily due to the Argyle mine, the largest source of rare pink diamonds in the world. “Lampraites were mined in Australia – this is a rock close to kimberlites, but with a number of differences. Argyle has been completely worked out, everything that could be squeezed out has already been squeezed out. Although there are kimberlite pipes in the region, the age of which varies greatly – from very ancient to relatively young,” explains Vladimir Shchukin. But industrial development is no longer being carried out – the country has left the race.

India – the birthplace of the world’s first diamond mining. Even in ancient times, stones were found here in placers, and legends about Golconda and great diamonds of indian origin became part of world history. Today the country preserves several ancient pipes, the age of which is estimated at 1.1 billion years, but the production volumes are small and they have no significance for the market.

Brazil became the first country after India where diamonds were found, and in the 18th–19th centuries led the market. At first these were alluvial deposits, but now kimberlite pipes are also being put into production. However, the country’s role is rather symbolic – as an important stage in history, rather than as an actual supplier.

Extraction is only half the battle

Mining diamonds is just the beginning. Next comes logistics, cutting, export and sales. And here, at the last stage, the main bottleneck now begins.

Russia continues production, but the market is choking. Cutters’ warehouses are overcrowded, there are no new buyers, and demand for jewelry in China and the United States is falling. This led to a crisis in India, the world cutting center. It was there that ALROSA sent most of its diamonds. In 2024, the import of raw materials into the country fell by 23%, export diamonds – by 25% in carats. This means that factories in India have begun to buy less raw materials for cutting – because they have no money, no orders and there is no point in purchasing new batches. And if there is no import, then there is nothing to process and nothing to sell – so exports also fall.

The situation is aggravated by other factors: banks have cut lending, factories have nothing to buy new batches with. As a result raw materials are accumulated from suppliers, and more and more processed stones remain in warehouses – they simply are not bought. “If India is up, it means the whole market is up,” sums up Vladimir Shchukin. This is not just a local failure, but a systemic failure of the entire global distribution chain.

Additional pressure is created by artificial diamonds: they are cheaper, cleaner, and there are more and more of them. For some buyers, this is a reasonable alternative, especially in times of economic uncertainty.

Synthetic diamonds: why mine if you can grow them?

Why mine diamonds at all if you can now grow them in a laboratory? Fast, accurate, without mines and billions of dollars in investments. If synthetics are cleaner, cheaper and visually indistinguishable from natural stone, wouldn’t it be easier to just switch to it? Let’s figure it out.

Yes, technology has come a long way. “A recent achievement is growing large crystals. Previously, this was impossible, but now they have learned to create even ten-carat ones. However, the process remains very lengthy,” explains Vladimir Shchukin.

Still, synthetics are not a complete replacement. Although it is already replacing natural diamonds in industrial applications – for example, in cutting tools – in electronics and especially in jewelry, natural crystals are still unrivaled. However, it is not only a matter of physical properties, but also of perception: natural stone remains a symbol of rarity and true value.

“The secret is that the growth in the production of artificial diamonds has almost no effect on the sales of natural ones. It’s clear to everyone: natural stone carries a special value and emotion that is inaccessible to synthetics,” says Shchukin.

Natural diamond is not just a mineral. This is history, rarity, symbol. And as long as a person values nature and authenticity, diamonds mined from the depths will have their place.

Who else influences the market: De Beers and supply policy

In addition to producing countries, the market is also influenced by large structures that control supply. De Beers has long played one of the most prominent roles in diamond policy. Vladimir Shchukin tells how this happened:

“When diamond mining was carried out only in Yakutia, and beautiful stones were mined there, De Beers was actually in charge of this process. All diamonds were sold through them. How did it work? De Beers collected diamonds in so-called boxes – boxes with a certain set of stones. Botswana diamonds were added to these boxes, which cost modestly – about 50-60 dollars per carat, and Yakut diamonds were mixed in, with an average price of 110-140 dollars per carat. This mix allowed them to sell the product profitably, turning it all into a great business.”

Shchukin also recalls how De Beers influenced Russian fields:

“The discovery [of Lomonosovsky] took place in 1996 thanks to the participation of foreign investors, among whom De Beers was active. They seem to have received permission from the government and initiated additional exploration using their methodology to convince foreign partners of the project’s potential. But the launch was delayed until 2014 – this was an obvious delay. Most likely, the goal was to delay the commissioning of both the Lomonosovsky and the Grib pipes for as long as possible – to prevent excess carats from entering the market and to prevent prices from collapsing.”

These steps caused mistrust among Russian geologists. Today, Shchukin emphasizes, the return of De Beers to Russia is excluded: “Now no one will let players like De Beers come here. This is no longer a question of geology, but of sovereignty. The law excludes such tolerances – and rightly so.”

He also notes that the company’s influence as a whole remains: “De Beers and Anglo American are working stably, without reducing volumes, although rumors about the sale of assets due to the difficult situation have been circulating for a long time.” Now the company’s focus has shifted to Africa and Canada. But for Russia this is already the story of a bygone era.

Sanctions and geopolitics: a challenge for ALROSA diamonds

Today ALROSA is one of the largest diamond producers in the world – works under double pressure conditions. On the one hand, sanctions have limited access to foreign markets and technologies. On the other hand, long-standing infrastructural and technological problems are worsening within the country.

According to Vladimir Shchukin, sanctions became especially sensitive after the loss of the markets where the main sales traditionally went. Example – Angola: Catoca pipe, where it previously participated ALROSA, came under the control of other players. This has increased price pressure: at international auctions, Russian diamonds are now sold at discounts of up to 15–20%. Such conditions affect not only revenues, but also the exploration budget.

Within the company, the problems are no less acute. Modernization is proceeding unevenly: in some places, like at the Grib pipe, AI systems and modern enrichment technologies have been introduced, but most of the assets still operate with outdated equipment. PosTawki Western decisions are blocked, import substitution is proceeding slowly.

A separate topic is infrastructure. Many mines were built in Soviet times and require major repairs, updated ventilation, and replacement of communications. All this despite the high cost of working in permafrost. The new project “Deep World” is an attempt to revive production at one of the most important pipes that was sunk in 2017. But implementation requires large-scale construction: a concrete plug, drainage, and sinking a new shaft. Engineering risks remain.

However, the company is adapting. Shchukin notes that ALROSA is working more actively with India – now it is a key market. Even the least marketable goods go there for cutting. Indian craftsmen collect several small stones into one, obtaining diamonds up to a carat. This does not save the market as a whole, but it helps to stay afloat.

There are prospects – if we continue to focus on flexibility, look for new sales channels and in parallel build up internal technological stability. “As long as a company can quickly adapt to conditions, it has a chance,” says Shchukin.

What’s next: disappearance or transformation?

Today, the diamond market is experiencing a shift: global reserves are dwindling, demand for jewelry is declining, and synthetics are conquering the mass segment. The buyer has become more careful, and the old model – “mined and sold” – no longer works. The world is shaking not only because of sanctions against individual countries, but because of a change in the entire logic of the market.

Against this background, Russia also found itself under pressure: sanctions, reorientation of logistics, internal infrastructure challenges. But all this is part of the big picture. The system dominated by natural diamonds is going away. A new era is dawning.

But this is not the end. Natural diamonds remain valuable – as carriers of unique properties, as emotionally charged symbols, as material for high technology. Synthetics do not cancel them, it just occupies a different niche.

Intelligence remains key. But, as Vladimir Shchukin emphasizes, now it is not only geology, but also strategy. “The focus should be on technology, competent exploration and understanding why we mine diamonds,” he says.

The diamond industry is not disappearing – it is being rebuilt. Those who can change, think in segments, and look for value, not just volume, will win. We are facing not a decline, but a new chapter.

Is diamond mining a passing era or is it still a stable market of the future? Will synthetics replace natural stones – or will they retain their unique value? Write in the comments – let’s figure it out together.

The material was prepared with the support of the Russian Ministry of Education and Science as part of the Decade of Science and Technology