Gold is in price, reports sound confident, investors are entering the industry. And inside there is a staff shortage, pressure on small players and a chain of transactions in which companies are rushing to get rid of non-core assets. Large businesses are reassembling their portfolios, there is a wave of mergers and sales, small businesses are barely surviving under administrative pressure, and the junior sector has still not been able to fully form. At the same time, record profits threaten to result in a new fiscal burden – and instead of development, the industry is increasingly falling back into survival mode.

At the conference of the magazine “Gold and Technologies” gave an overview of trends Mikhail Leskov — editor-in-chief of the magazine, an expert with more than 30 years of experience in the mining industry, consultant and participant in dozens of projects in Russia, the CIS, Asia and Africa. We’re publishing his speech in column format just as it was delivered, and we’ve added some editorial notes on the numbers to explain how they compare to the industry picture.

Disclaimer: There are no official open statistics for Russia. All figures given in the column are expert estimates compiled and cross-checked based on available data. The expert is confident in their reliability, but we ask you to treat them with reasonable caution.

Record prices, slowing production and rising costs

Gold prices continue to rise steadily in 2024–2025. In the third in the ten days of April 2025 they reached USD 3401.4 per ounce (against USD 2391.2 a year earlier), and June futures exceeded USD 3500. The growth has been going on for more than two years, and so far there are no obvious reasons that could stop it. Previous economic and geopolitical forecasting models have stopped working – the turbulence of world markets makes the future difficult to predict.

Against this background, for the first time in a long time, a slowdown in global gold mining. According to preliminary but confirmed data, global production has decreased. Of the Top 5 countries, only China showed growth, while Russia maintained the same level – about 345 tons, maintaining second place in the world.

At the same time, the decline in production against the backdrop of high prices looks paradoxical, but is explained by the inertia of the industry: the launch of new projects takes time, the response to demand is always late. At the same time, global production costs are rising. Russia is still one of the countries with low dollar costs, but within the country ruble costs are growing rapidly, which significantly affects the economy of companies.

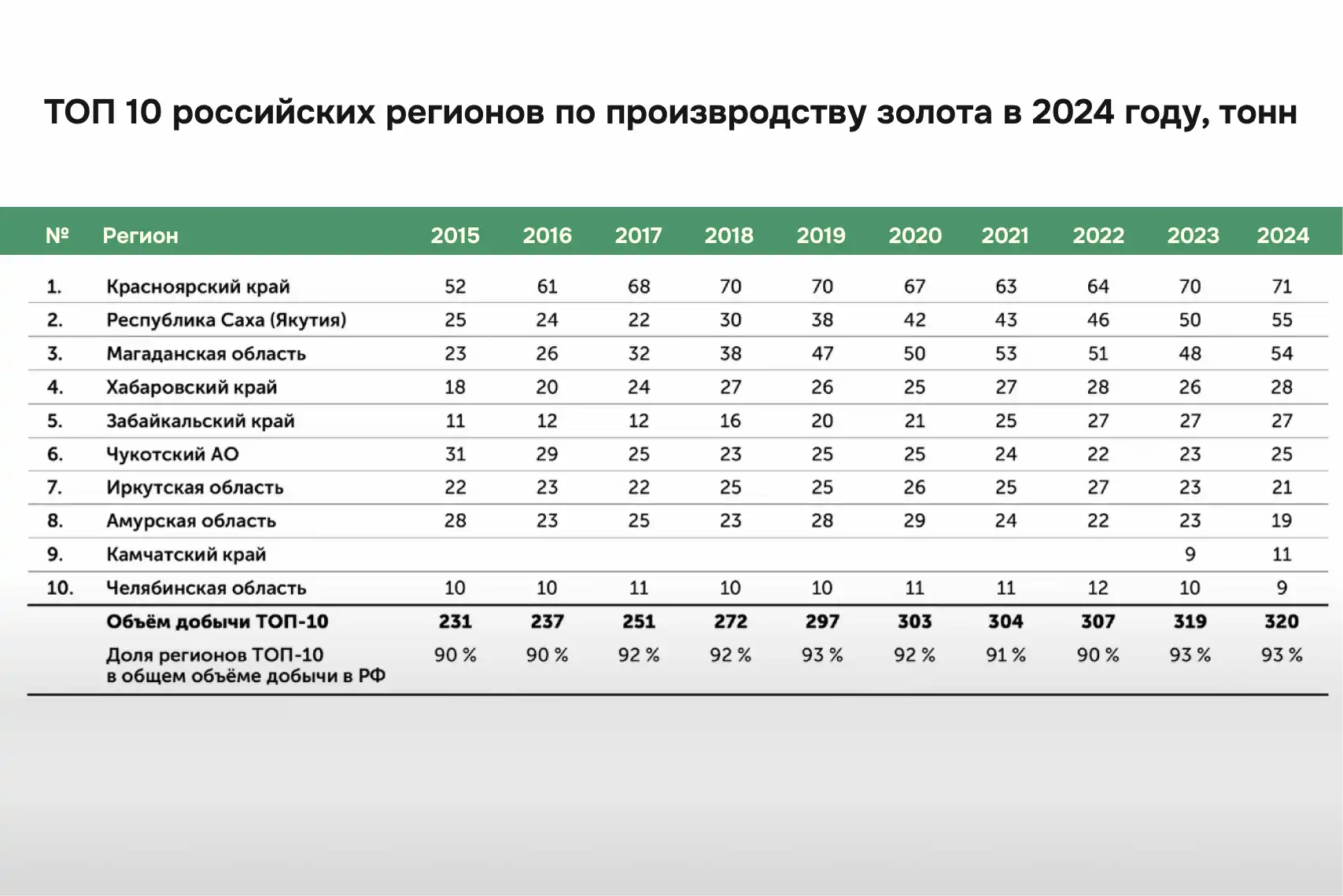

Production volumes: Russia maintains its position

At the end of 2024, Russia remains in second place in terms of gold production in the world – about 345 tons, which is almost the same as last year. The growth has been recorded, but it is minimal, within the limits of statistical error.

By comparison, most other countries are in decline. China is the only exception, but its statistics are traditionally updated at the end of next year, and, as a rule, downward. Therefore, it is possible that in the final figures Russia will again rise to first place, as it already did, for example, in 2021. According to Metals Focus, USGS and analysts from Gold and Technology magazine, total global production in 2024 amounted to 3,625 tons, which is slightly lower than the level of 2023 (3,644 tons) and almost equal to 2022.

In 2024, the activity of Russian companies in the field of mergers and acquisitions continued to grow. Based on the results of this year’s transactions, we can expect noticeable changes in the ranking of the largest gold mining companies in Russia. At the same time, the activities of junior, as well as small and medium-sized mining companies intensified. This, along with rising prices, has stimulated an increase in exploration budgets – according to preliminary data, they have increased again compared to 2023.

Regional picture: who added and who lost ground

Let’s look at how gold production has changed in different regions of Russia at the end of 2024. In some places it was possible to increase volumes, in others, on the contrary, there was a noticeable decline. The eastern regions continue to determine the face of the industry, but the dynamics within them are very heterogeneous. Compared to 2023, in 2024:

Showed strong growth:

- Republic of Sakha (Yakutia): +5 t (from 50 to 55 t)

- Magadan region: +6 t (from 48 to 54 t)

- Kamchatka: +2 t (from 9 to 11 t)

- Khabarovsk Territory: +1 t (from 27 to 28 t)

The decrease was recorded in:

- Amur region: −4 t (from 23 to 19 t)

- Irkutsk region: −2 t (from 25 to 23 t)

- Chelyabinsk region: −3 t (from 12 to 9 t)

Changes by region are clearly visible on comparative maps: if in 2023 the decline was noticeable in the Magadan and Khabarovsk territories, then in 2024 they both show growth, compensating for last year’s losses. In turn, the Amur and Chelyabinsk regions went into deep negative territory.

Top ranking lines: no change of leaders

Now let’s see how the positions at the top of the regional ranking in terms of production volumes are distributed. Here, in contrast to the middle of the table, almost no changes occurred. The top three remained the same:

- Krasnoyarsk Territory – 71 t

- Republic of Sakha (Yakutia) – 55 t

- Magadan region – 54 t

Although Yakutia and the Magadan region continue to change places in the ranking (in 2022 Yakutia was second, in 2023 – Magadan, in 2024 Yakutia again). The gap between regions is minimal, and changing positions is not a matter of strategy, but the result of annual fluctuations in production volumes. Other notable movements:

- Kamchatka region strengthened its position in the top ten, finally displacing the Chelyabinsk region, which in 2024 was in 10th place with a volume of only 9 tons. This is a noticeable shift: Kamchatka is consistently increasing production for the second year in a row, and although its contribution to the overall picture is still relatively modest, it shows potential for development – unlike regions where volumes are declining. This is especially important to understand: the key gold-mining territories include a region that was not included there until recently.

- Total production volume by TOP 10 regions increased to 320 tons, while the share of the TOP-10 in total production in the country remained at 93%, as in 2023. This means that no influx of new active regions has occurred, and the main load continues to lie in the same largest territories.

Rating of companies: who held their positions, who lost, who entered for the first time

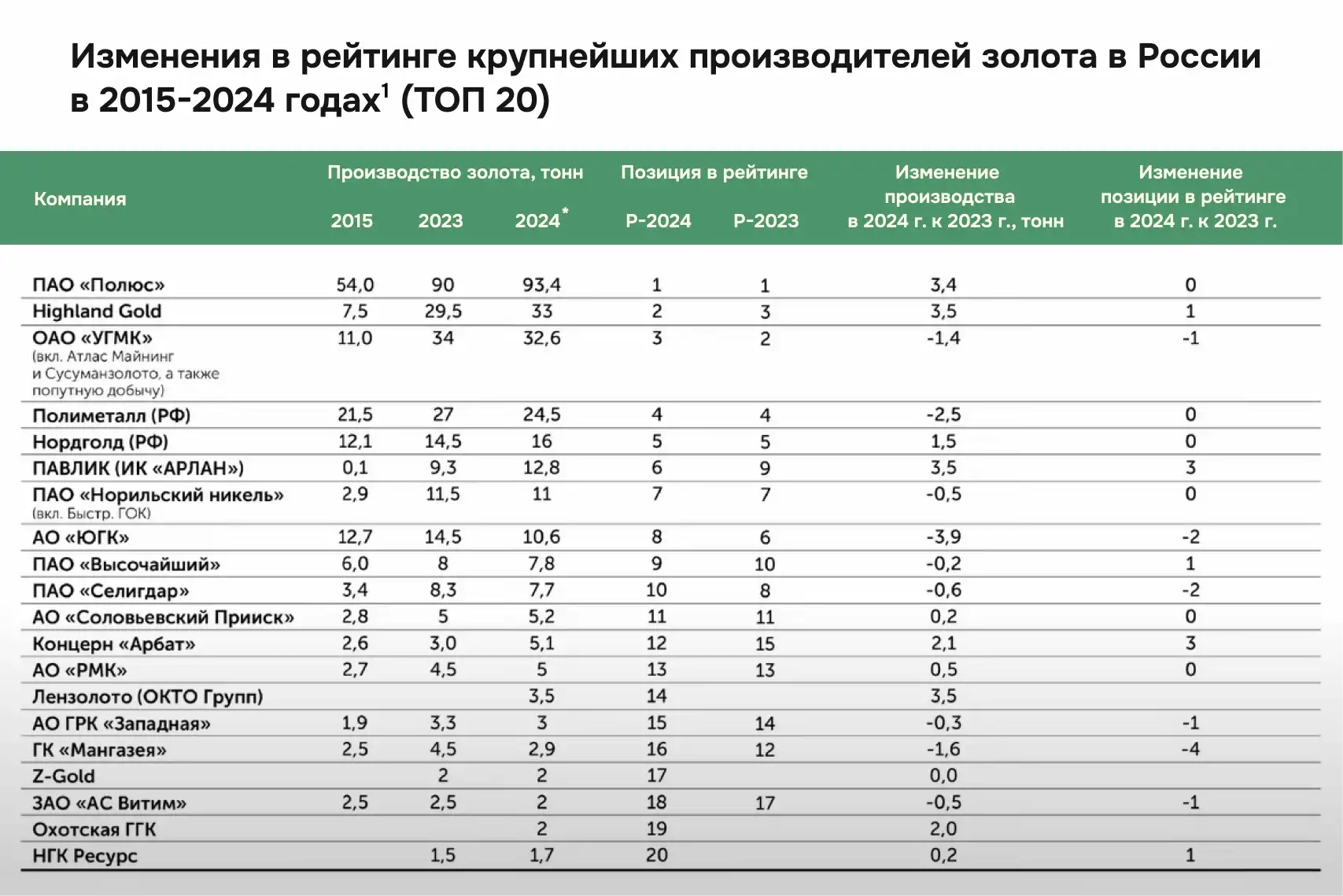

Now let’s move on to the results by company. Below is a table of the largest gold producers in Russia based on the results of 2024. But it’s worth making a reservation right away: the rating was compiled taking into account a number of assumptions, because a number of assets changed owners, and the data remains partially closed.

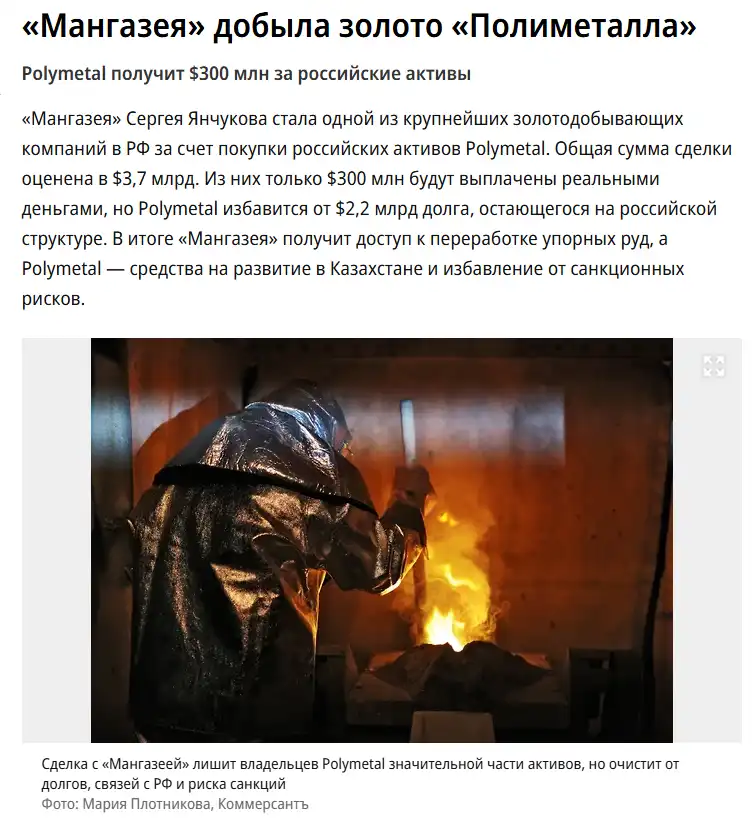

One of the main assumptions is related to Polymetal: in 2024, its Russian assets officially came under the control of the Mangazeya Group of Companies, but at the request of the latter, they are listed separately in the table. Therefore, JSC Polymetal (RF) and GC Mangazeya are presented as two separate lines. If we combine the data of JSC Polymetal (RF) and GC Mangazeya (which is logical, given the transfer of assets and management succession), then instead of two lines in the table there will be one – and then there will be a total of 19 companies in the rating. In this case, the Zolotoy Aktiv company takes 20th place, which in 2024 acquired the Ozernovskoye deposit in Kamchatka from Sigma and produced 1.6 tons of gold. It is not formally presented in the table, but in terms of volume it is fully within the top twenty.

Rating leaders and changes

- PJSC Polyus confidently retains first place: 93.4 tons (+3.4 tons compared to last year), despite the fact that in 2024 the company sold a number of assets. This means that growth on the remaining sites was even higher.

- Highland Gold rose to second place for the first time (33 t, +3.5 t).

- OJSC “UMMC” (incl. Atlas Mining and Susumanzoloto) moved from 2nd to 3rd place with a slight decrease (-1.4 tons).

Among the companies that improved their positions:

- PAVLIK (IC “ARLAN”): +3.5 t, rose to 6th place.

- Concern “Arbat”: +2.1 t, improved the position by 3 lines at once.

- JSC RMK And Lenzoloto (OKTO Group) – also a plus.

Who sank

- JSC “UGK”: −3.9 t, fell from 8th to 10th place.

- JSC “Seligdar” And JSC “Vysochaishy” also showed a slight decrease.

- GC “Mangazeya”: −1.6 t and a drop of 4 positions – the largest pullback in the ranking.

Newcomers to the top twenty Congratulations Z-Gold And NGK Resurs — both companies entered the TOP 20 for the first time:

- Z-Gold – thanks to the consolidation of assets in Buryatia (Zun-Kholba, Irokinda, etc.).

- NGK Resurs — by increasing volumes and modernizing the Polyanka field.

It is important to note again that actual data for a number of companies is not available. All that is presented are estimates based on retrospective analysis and open sources. During the year, many opaque corporate events took place. Who sold what to whom, who is the final beneficiary, and who is just transit – often remains unclear. This complicates the ranking.

General indicators for the twenty

- The total production volume of the companies from the table is about 248 tons, almost the same as in 2023. This means that the industry as a whole has not increased production, despite high prices and continued investor interest. There is no growth either at the expense of old players or at the expense of new ones – which emphasizes the inertia and internal tension of the current model.

- The threshold for entering the top ten decreased from 8.5 tons to 7.7 tons. If we count Polymetal and Mangazeya together, it is even lower, just over 5 tons.

- Half of the companies in the table have a placer component in their production. But in 2023 there were 13 of these out of 20. In 2024 there were only 9. This suggests that even large players began to consistently abandon alluvial assets, displacing it as a lower priority.

- At the same time, the general downward trend is intensifying: if in 2023 only 2 companies from the top ten showed a decrease in production, then in 2024 there were already 6 out of 10 such companies. This is a direct signal of declining sustainability even among industry leaders.

These shifts are not just an internal rearrangement of the table, but a sign of a profound restructuring of the entire industry. This is especially noticeable in the placer mining segment: even large companies are beginning to abandon it, considering such assets to be burdensome or insufficiently efficient.

At the same time, even among the industry leaders there are more and more of those who show a decline in production rather than an increase. This suggests that gold mining in Russia is becoming less and less like a sustainable system – and more and more like a field with unresolved structural problems.

As for the data on companies producing less than 100 kg per year – and this, by the way, is the largest part of gold miners in the country: about 700 companies, of which more than 400 produced less than 100 kg per year – the situation here is vague. Statistics for this segment have ceased to be published, and now we do not have a detailed invoice.

According to expert estimates, the number of such small companies has decreased significantly in 2023 and 2024, and everything indicates that the trend towards their disappearance will continue. We will talk about the consequences of this trend separately, but we can already say: the industry is losing small players, and this is noticeable on the overall production map.

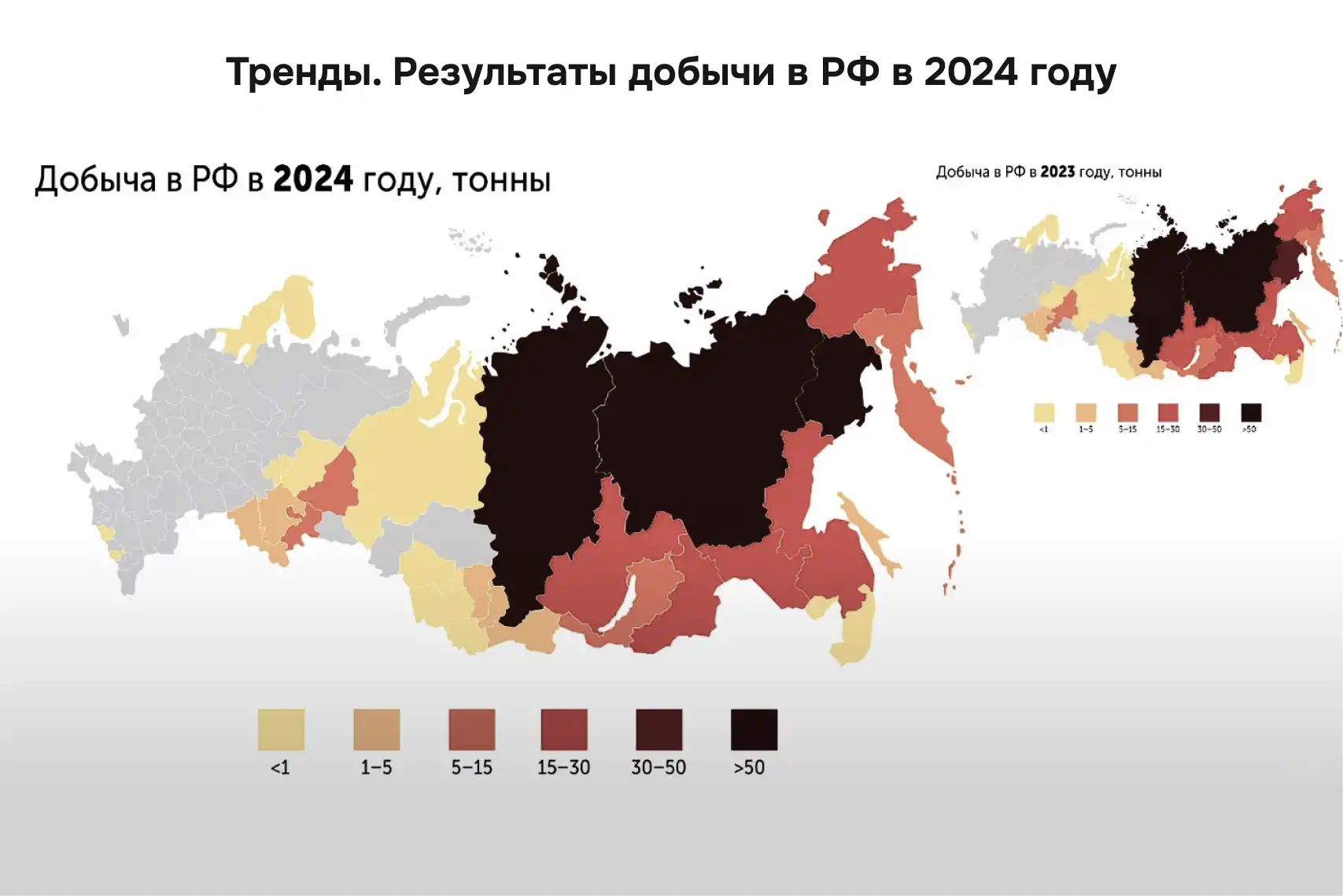

Geography of production: growth without expansion

If you look at the map of gold mining in Russia for 2024 (compared to 2023), you can see: the main volumes are still concentrated in the eastern part of the country – Eastern Siberia, the Far East. This is not a new observation, but it is only confirmed year after year.

- Darker tones on the map are regions with more loot.

- In 2024, there are only three such regions – these are those that are included in the “over 50 tons” category:

• Krasnoyarsk region

• Republic of Sakha (Yakutia)

• Magadan region

At the same time, in 2023 there was another active category in Russia – production from 30 to 50 tons, which was represented by the Magadan region. Now she has moved to the highest category, and the intermediate zone has simply disappeared. Visually, this makes the map more contrast, but essentially shows that the gap between the leaders and the rest has increased.

In 2023, there were six regions in the “medium” production category (about 20 tons). In 2024, there were five of them left – the Amur region dropped out, showing a noticeable decrease. This suggests that the second echelon of regions is not yet strengthening. However, a number of territories are on the verge of moving to a higher category – they are, as they say, supporting the next level.

As the expert noted, there is hope that some of these regions will be able to increase volumes and in the future enter the category with production of over 20 tons. Not right away, not this year, but they have potential, and the picture may still change.

Key events 2024: sales, launches, shake-ups

In 2024, gold mining in Russia was in a state of constant change. Assets changed hands, new deposits were launched, and megaprojects with associated gold gained momentum. At the same time, the industry was faced with accidents, regulatory pressure and suffocating lending rates. These events do not just shape the current picture – they set the contours of tomorrow. Let’s sort them out into blocks.

Market redistribution: who is leaving, who is entering and why

One of the main trends of the year is the active reshaping of portfolios. First of all, this is, of course, the transfer of Russian assets Polymetal under the control of Mangazeya Mining. Next is the sale by Polyus of the Bamskoye deposit to Atlas Mining, the transfer GDK Degdekan in the structure of Alrosa, the transfer of Lenzoloto under the wing of the OKTO group and other similar transactions.

What’s behind this? Essentially, large companies have reached the limit of their growth. That very “limitless” one, which, as it turns out, was never such. By the way, this is not only Russian history – the same thing is happening abroad. When a company grows to a certain scale, it begins to think not about expansion, but about efficiency: corporate costs, manageability, profitability of individual assets. If an asset becomes non-core or falls out of priority, it leaves the structure.

Simply put, a company that has outgrown its “short pants” passes them on to someone else to wear. And this is a completely working scheme. Let’s remember: in 2006, Polymetal bought the Kubaka deposit from Kinross. Then the project was considered exhausted: the tailings dump was reclaimed, gold cost $650 per ounce – everything was heading towards closure. But 19 years have passed, and the Omolon hub not only works, it maintains stable volumes. As it turned out, the pants were not short at all.

Maybe someday the time will come for the Omolon hub to change its owner. But for now this is a living, working project – and it shows that the transfer of assets “down the chain” can be meaningful: it can be restarted, modified, adapted. The same thing happened with the Nezhdaninsky deposit: Polyus considered it not a priority, sold it to Polymetal, and it quickly put it into operation.

And such cases are likely to be repeated. Large players have already formed voluminous and diverse portfolios. And it is obvious: those assets that occupy the bottom line in the list of priorities will leave – creating new opportunities for transactions, mergers, and relaunches. Another important thing is that these deals open up the entry of new players. As, for example, the OKTO group did. She didn’t just enter the industry—she established herself, and, I must say, quite confidently.

Launched: from Sukhoi Log to Baimka – where more

Positive events include the start of development of Sukhoi Log ores by the Polyus company. This is truly a significant moment: yes, while we are talking about the processing of mined ores at the facilities of the Verninsky gold processing plant, but still, this is actually the start of industrial development of the largest gold deposit in Eurasia. The event is extremely important for the industry.

The launch of production at the Vysokoye deposit in the Krasnoyarsk Territory, where Yuzhuralzoloto operates, also had a serious impact on the overall picture. Four-million-dollar deposits—the so-called deposits with a resource base of more than 4 million ounces (that is, over 120 tons)—are launched in gold mining infrequently. And if the launch was also quick and successful, then this is truly an event. Considering that the company is simultaneously implementing several other projects, we can expect further growth from it.

We should not forget about mega-constructions at large complex sites with associated gold. Formally, these are not gold mining projects, but their associated production volumes are very significant. Thus, Malmyzh is expected to produce about 20 tons of gold per year. Baimsky GOK on Peschanka, most likely, it will add about the same amount. Kultum will also provide significant volumes, at the level of “many tons,” let’s say. And this is just the tip of the iceberg. These projects are already contributing to overall production – and this contribution, apparently, will only increase.

But, of course, the events in the industry were not only positive – there were also those that significantly affected indicators and sentiment. More about them later.

Accidents, rates, turbulence: where the industry is slowing down

Among the negative events, it is difficult not to note the suspension of production at the Chelyabinsk quarries of Yuzhuralzoloto for as much as 90 days. This significantly impacted not only the performance of the company itself, but also the overall production volume in the Chelyabinsk region. The accident at the Pioneer mine at Atlas Mining, as well as a number of other similar cases, also had a significant impact on industry figures. Taken together, all this was reflected in both general industry statistics and growth dynamics, which – if in previous years it was “fast” – has now slowed down to almost imperceptible.

It is important to understand: these are not only causes, but also consequences. The consequences of other, more profound processes – we will return to them a little later.

Separate line – credit rates. We can say that the year was “famous” for them – alas, in quotes. High borrowing costs have dealt a severe blow to companies’ investment plans. Reconstruction projects, capacity expansion, new transactions – all this has become much more difficult to implement.

Yes, the rising price of gold partially mitigates the situation. But – that’s exactly what is partial. And not forever: the trend can reverse at any moment. But credit rates, alas, are still with us – and they set the current climate for the development of the industry

There is potential. What about the possibilities?

As for the prerequisites for further forecasts. For now, we assume that gold exploration and mining continues to be one of the most attractive areas for investors, especially compared to other industries within the country. We see steady interest, including from players from related sectors. This is not the story of one year – interest has been ongoing for several years and, moreover, is only growing. This is likely to spur increased competition in the industry.

But we must understand: along with this, sectoral inflation will also grow. Everything – from labor to equipment, materials, logistics and services – will become more expensive. And, apparently, at a fairly fast pace.

The most acute shortage of personnel is felt. And not only quantitative, but also qualitative: There is a shortage of not just people, but people with the required qualifications. This is already a chronic problem that requires companies to increase productivity and efficiency – and, accordingly, additional investments.

Other restrictions also remain: high lending rates and poor development of equity financing mechanisms. So far, few people go to the stock exchange to attract investments through the sale of shares (equity) – and this could be a more budget-friendly instrument than loans. But this route is still poorly accessible for mining companies.

And finally, another difficulty is the closed nature of the country. Equipment, technology, materials, engineering knowledge – access to all this is now limited. Not completely, but still with additional costs and time. And this certainly affects the industry’s ability to move forward.

Trends in gold mining in Russia

Gold mining in Russia is changing – and not always according to the scenario that seems obvious against the backdrop of high prices. Which areas are strengthening, who is leaving the market, and what will determine the sustainability of the industry in the coming years? Let’s look at four key trends

Placer mining – endangered

One of the most alarming trends is the tightening of conditions for placer mining. Moreover, it is especially ironic that exactly those departments that, it would seem, were supposed to support this area, were doing this. But in practice – either through thoughtlessness or quite deliberately – they consistently complicate life for that part of the industry that is already struggling to survive.

But it is precisely this “trifle” – companies that mine tens of kilograms of gold per year – that forms the very elementary school of the industry. Yes it is troublesome people, yes, they sometimes break something, don’t comply with something. But it is there that future personnel for all gold mining study, gain experience and hone their craft. If this segment is cut off, the source of people who are already sorely lacking will disappear.

There is one more point: without this segment, most of the geological exploration will collapse. Simply because no one else will go to those areas where prospectors now travel on winter roads – not for any money. This is a unique and, in many ways, the last way to maintain the development of hard-to-reach territories. Now it’s the small and troublesome subsoil users who are doing this—the same ones who, if you’ll excuse the expression, are consistently screwed up in our country.

I would like to see a reversal of this trend. But for now – alas – it is only getting stronger.

Associated gold production – strong growth

One of the positive trends is the growing interest in the associated extraction of gold from complex raw materials. This applies not only to non-ferrous metals, but also to such areas as the mining of uranium and other minerals, during the processing of which gold can be extracted in parallel.

The rise in gold prices stimulates a more active involvement in the processing of those ores that were previously either not considered at all as a source of precious metal, or were considered too “persistent” and difficult to extract. Now they are being involved more actively – and this gives the industry new sources of growth.

The variety of industries focused on processing concentrates will also expand. The volume of movement of intermediate products between enterprises within the country will also continue to grow – this trend is already noticeable, and, apparently, will only intensify.

(Editor’s note: we are talking about transporting intermediate products – for example, gold concentrates – from one enterprise to another. This allows us not to build expensive processing at each deposit, but to use existing capacities and more advanced extraction technologies. This approach reduces capital and operating costs, minimizes metal losses and makes the industry more flexible and sustainable.)

Resource hunger remains – but juniors are starting to wake up

Despite the cheerful reports on the increase in reserves, the actual exploration reserve remains insufficient – the increases are not happening where they are most needed. The hunger for resources is no worse than the shortage of personnel.

However, there is a positive change: The junior sector is starting to revive. Interest in early-stage projects is growing, and not only large mining companies, but also external investors are beginning to participate in financing. This could mean the beginning of a turning point – and perhaps the trend will change direction in the medium term.

New players are entering the industry, albeit with old names

The trend of influx of “new” players into the industry continues to gain momentum. Why is “new” in quotes? Because often these are companies or entrepreneurs that have been working successfully in related sectors for a long time, but have not previously participated in gold mining. Now they are entering the industry: some with an interest in transactions, others with an attempt to gain a foothold in production.

There are successful examples of entry, and there are not so good ones. But each of them – even with mistakes – forms an experience that helps you move on more effectively. And this interest in itself shows: gold is still perceived as an attractive direction, despite all the difficulties.

Conclusions: the industry is holding on – but at the limit

The dynamics of the recovery of gold mining after the shocks of 2022 showed that the industry as a whole is coping well with the challenges. In 2023, a recovery in volumes was recorded. But 2024 brought new challenges: despite a record gold price and an influx of interest, we see overheating, project acceleration and unsustainable business models. This leads to companies and investors making decisions based on emotions and haste – and not always successfully.

We are already seeing the consequences of this race: the stoppage of Yuzhuralzoloto’s work at the Chelyabinsk quarries, accident at the Pioneer mine at Atlas Mining and a number of smaller companies are in trouble. These stories rarely become public, but accumulate in the professional field – and can be repeated if they are not comprehended and discussed.

Formally, the country is not losing ground in terms of volume. Russia is still in second place in the world, and in the 2027–2030 period it still has a chance to return to first place. However, behind the beautiful figure lies a decrease in sustainability: the economy of many even large companies is deteriorating. High lending rates, rising costs, unstable exchange rates and regulatory uncertainty make long-term planning almost impossible.

That is why peak excess profits, which now arise due to high prices, cannot be perceived as “extra.” This is the only chance to create a “plan B”: a safety cushion in the event of a drop in prices, an increase in the exchange rate, or a further increase in the cost of borrowing. To withdraw this money now would undermine the already strained sustainability of the industry.

At the same time, geological exploration will continue to intensify. The main emphasis will be on medium-sized deposits – 20-30 tons, with clear logistics and acceptable investment risks. This is a sober, realistic strategy in an environment where super-large facilities are almost impossible to finance.

And most importantly. The industry needs stop being silent. Successes, failures, mistakes, breakdowns – all this is part of reality. And if you don’t talk about it, if you don’t share cases, even complex ones, it means depriving others of the opportunity to avoid the same mistakes. There were, are and will be difficulties. But only an open professional discussion can give the industry immunity from repeating its own rake.

The material was prepared with the support of the Russian Ministry of Education and Science as part of the Decade of Science and Technology